Sometimes things come together all at once and that is the case for this essay. As I was finishing up edits for my book project The Engineers: A Western New York Basketball Story, I did a broadcast on my science and technology YouTube channel for Black History Month. It focused on the Physicist Dr. Sylvester James Gates, Jr. and his peers. I started the broadcast by noting that I struggled with Physics during my junior year of high school, an important part of the story arc in my book.

I further noted that having the right Physics teacher can make all the difference in the world. Dr. Gates stated the same thing in the interview with him I read during the broadcast. He shared that an early Physics teacher inspired him to start his storied journey using an intriguing physics demonstration/experiment for he and his classmates. The sum of all of this was the genesis for this essay discussing learning Physics, and the critical role teachers play when giving instruction on the Grandfather of all the sciences.

The Grandfather of the Sciences

Physics is often referred to as the Grandfather of all of the sciences. I recall hearing that somewhere. Simply put, this just means that Physics is the basis for all of the other sciences. While my doctorate is in Pharmacology, Physics touched every aspect of my graduate research at the University of Michigan. My thesis project asked questions about drugs and their effects in living systems. That said all of the instruments we used to ask those questions used physics-based principles in one way or another. That goes for our columns used for chromatography, our orbital shakers, our mass spectrometers, our 96-well microtiter plate reader, our high performance liquid chromatography (HPLC) devices, etc. In short, no matter the science or application, Physics touches it.

My High School Physics Teacher

My Physics teacher at Hutch-Tech High School six years earlier was Mr. Kenneth Boudreau. As you can deduce from his name he was of French descent. He was a skinny man who typically wore a white button down shirt, fitted black slacks and black shoes. He had gray hair, a gray beard and wore glasses. He could have been your stereotypical government scientist at NASA or any observatory. Everyday he brought a thermos to class and seemed to be wired on caffeine. A classmate actually joked once that he never blinked. Finally I noticed that he frequently popped chewable antacids in his mouth. He was in fact robot-like and spoke in a monotone way.

Our Teacher’s Level of Effectiveness

“It is that simple folks!” Every time Mr. Boudreau explained something to us or showed us a calculation on the board, he ended by enthusiastically saying, “It is that simple!” I only remember a few things from that entire year under his instruction. I remember an initial lesson on scalars and vectors. I also remember hearing the word Mechanics which was the chapter dealing with the movement of objects, impulses and velocities. I am certain the Electrical Technology and Mechanical Technology majors at Hutch-Tech remember more. They had to as Physics was the basis of their majors. The Electrical Engineering majors particularly had to understand electrical potentials, currents and resistance.

“Is there a way you can make this more exciting and interesting?” I also recall a classmate asking our teacher potentially the most important part of learning Physics, especially for beginners. As described later, Physics is a calculation intensive science and unless you know why you are doing those calculations, it is easy to get lost. While our teacher knew his calculations and formulas, there were not many demonstrations so we could see their applications.

By the way I am not sharing these stories to beat up on Mr. Boudreau. As I will describe later, he did something very important for me towards the end of that year. That said, making classroom material interesting is a larger educational skill and transcends Physics. It goes for pretty much every subject.

I also struggled with Physical Science in the eighth grade at Campus West, the precursor to Physics. The teacher was also a little on the dry side. He shared the same last name as a famous singer from the group ‘The Rat Pack’ whose first name was Frank. Okay it was Dr. Sinatra. I excelled at Life Science the previous year under another teacher who brought a lot of enthusiasm and creativity to our classes. That was Mr. Radamacher. My undergraduate Physics professor at Johnson C. Smith University also did not make the subject particularly interesting either but at that point, I knew how to approach the class.

Early Struggles and Gradual Progress

My junior year was marked by a mysterious injury suffered when running cross-country, a basketball season that came off the rails, and struggles in both Course 3 Math and Physics. While I struggled early in Physics, my math grade was average but dipped during the adversity from my basketball season. After my basketball season came to its early finish, my math grade rebounded once I refocused.

“Physics is a different way of looking at the world,” my father said over the phone during my struggles. He majored in Physics in college but there was minimal help he could give from five hours away with no internet. I did not understand his riddle immediately but I eventually figured it out.

My progress in Physics was incremental after starting off with a grade in the high 60s after that first semester. As described in my essay entitled, The Keys To Learning College Level Physics, once I sat down and started going over the materials and the problems, things started making sense. I wrote a similar piece about Chemistry. Physics was a quantitative science and it was calculation intensive. There was a formula for most of the principles whether it was a car accelerating or a rocket jettisoning into space. Once you understood the principles you could identify which formula to use. You could then plug in the numbers given in the word problem. Oh yes, all of the problems were word problems, so reading comprehension was also critical. Afterwards it was simple Algebra as Mr. Boudreau stated.

Turning Things Around

“I want to congratulate you for turning things around this year! You have made a lot of progress!” Late in the year, Mr. Boudreau sought me out in one of our classes. I sat in the back of the room goofing off with some classmates. He watched me struggle in his class early that year. He further observed when the switch turned on for me and when I started to understand things. I did not become the top student in the class by any means, but I was no longer scraping the bottom either. His acknowledgement of my progress was his greatest gift to me from teacher to student. It was an encouragement that I never forgot. It was an important step for me academically and in my future education and career as a scientist.

Understanding the Applications of Physics

As I end this essay, I want to acknowledge that teaching is one of the hardest professions out there. It can be exponentially more difficult depending on the district you are in and the students you have. It is a profession I do not know if I have the patience for. There are several factors that go into how well a student performs in a particular class. The teacher is just one of them. In some instances outside factors can impact how students learn. In some instances like mine, the seeds are planted early but do not bloom until later.

Regardless, for a class like Physics, I think using real world applications is critical for learning it, especially for beginners. Years later while volunteering at the David M. Brown Arlington Planetarium, I saw firsthand why planetariums and fulldome shows are important, especially for young people. I further understood the advantages kids who attend them regularly have over those who do not. Planetariums and fulldome shows about outer space spark curiosity and the imagination. They also show how subjects like Physics are applied. They show that the calculations can be fun.

One such kid who got to attend a planetarium regularly was Raphael Perrino. I met Raphael through his father Ralph whose tutoring company I worked in for a little while. Eventually all three of us worked together while volunteering in the group, The Friends of Arlington’s David M. Brown Planetarium. After finishing his education, Raphael started working in the aerospace industry. He was gracious enough to agree to the interview on my science and technology YouTube channel below. Early in the discussion, he acknowledged his high school Physics teacher and trained actor Dean Howarth, another planetarium volunteer, for creatively, effectively and enthusiastically teaching him and his classmates.

Basketball, Physics and Life: What’s the Connection?

As discussed in the opening of this piece, my early struggles with Physics was a part of my early basketball journey chronicled in my two-part book project entitled, The Engineers: A Western New York Basketball Story. As I went through my struggles, my coach at the time Ken Jones suggested tutoring by one of our team captains who also did not finish out that year. He will remain anonymous. Me and this captain were not particularly close and when I called him seeking his help, he did not respond in a way that encouraged me to further pursue his help. I thus took a risk and decided to figure it out on my own.

When I look back on the whole thing, a couple of things come to mind. The first thing I think about is my lack of mental toughness. Our basketball season hung in the balance and I should have done whatever I needed to do to keep myself academically eligible even if it meant a little bit of joking and ridicule. It was a two-way street though, and the second thing I thought about is that winning teams are cohesive units that stick together. Thus If a teammate is struggling, it is important for teammates who have the ability to help, to help them for the good of the team.

Closing Words

This concludes this piece. Thank you for reading it if you did. Some of the images used in this essay were lifted from an issue of Understanding Physics. If you have a child or know one who is struggling in a course like Physics, you might also consider getting a tutor. As described earlier, I worked in the tutoring world for a little while. It was fun coaching struggling students up and it generated some extra income for me. Also consider visiting your local planetarium or nearby science demonstrations. You might help that struggling student by doing so, and you may inspire the next great scientist! Best regards.

The Big Words LLC Newsletter

For the next phase of my writing journey, I’m starting a monthly newsletter for my writing and video content creation company, the Big Words LLC. In it, I plan to share inspirational words, pieces from my writer’s blog and this blog, and select videos from my four YouTube channels. Finally, I will share updates for my book project The Engineers: A Western New York Basketball Story. Your personal information and privacy will be protected. Click this link and register using the sign-up button at the bottom of the announcement. If there is some issue signing up using the link provided, you can also email me at bwllcnl@gmail.com. Best regards.

This personal money story for Father’s Day 2022 discusses the subject of taxes and once again is inspired by my father. Here on the Big Words Blog Site, I’ve crafted several stories discussing how Dad’s sage wisdom has impacted my life, whether through a direct lesson, or from my observations of him. Some of his most poignant lessons have involved money and arguably created my love for financial literacy, though he and I don’t see eye to eye on everything money related today. One of Dad’s most important lessons involves an area that is the bane of some people’s existence, while being a pillar to the wealth-building strategy of others, taxes.

We’re All Playing One Big Financial Game

Recently it occurred to me that we’re all playing one big financial game, now a video game in our modern technological age. Certainly, money isn’t the sole key to happiness, but life is certainly better when you have an abundance of it versus a scarcity. I would thus define winning this game as having an abundance of it versus just scraping by and financially struggling. Among the factors that go into winning the game include: the family you come from, personal (and family) life choices, your financial IQ, personal grit or ambition, delaying gratification and your current environment.

Your financial IQ may be the most important of all the factors I listed, and it can be impacted by the other factors. This concept is covered in numerous books. Your financial IQ includes your ability to earn money, your ability to save money, your ability to invest money, your understanding of credit, your understanding of insurance and understanding taxes. If you’re born into a high financial IQ family, you will likely learn all these principles starting from the crib. If not, you must learn them along the way, if at all. Furthermore, learning them is going to be impacted by your own personal drive and curiosity. For now, let’s focus on many people’s least favorite topic, taxes.

Taxes: What They’re For And Paying Your Fair Share

First, I want to admit that I don’t know everything about taxes. I would highly encourage readers to subscribe to economist, Antony Davies’, YouTube channel entitled Words & Numbers. It’s one of my new favorite channels because it’s not politics driven, but instead economics and facts driven. I’m currently reading his and James Harrigan’s book, Cooperation and Coercion. Upon listening to his content, one of the things that you immediately start to understand is that our politicians are not always honest with us about who pays what and how much in terms of taxes. Furthermore, they’re not always clear about the ramifications for the tax changes they promote. Often, in the pursuit of a political office, they incite class warfare.

In any case, while some taxes are necessary for our municipal, state and federal governments to perform their tasks, there can be too many taxes and they can have harmful effects on everyone. Furthermore, a part of one’s financial health is managing your taxes. The more you read, learn and start understanding about money, the more you start learning that in our ‘progressive’ tax system, not everyone is taxed the same and there are a number of reasons why.

As extensively covered in the Rich Dad Poor Dad books, employees are taxed differently than businesses (small and large). As an employee, your tax burden changes the more earned income you generate, and you start to lose deductions the more your salary increases. In the above-mentioned Rich Dad books, there is a clear distinction between high income professionals and business owners, and each has different rules in our current tax code. As employees, one of your tools for diminishing taxes is tax deductible gifts or donations.

Tax Deductible Giving

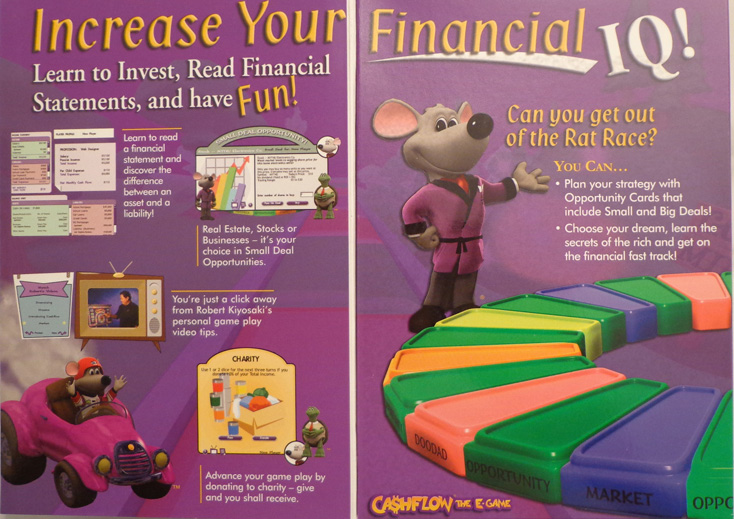

Around the time I moved in with Dad for my postdoctoral fellowship, a couple of things coalesced in my mind in this area. First, I got a copy of the Cashflow 101 e-game which I played regularly on my personal computer. Just briefly, the game is designed to teach you financial literacy and the goal is to get out of the ‘rat race‘ (the realm of working 9-5), and onto the ‘fast track‘, or the realm of the wealthy, where you can live on your investments and pursue your dreams. One of the things I realized when playing the game was that the rat race contained yellow ’donation’ squares. When you landed on those squares, you had the option of donating money.

If you chose this option, you received extra rolls of the dice with multiple dice. I refused the option initially and then realized that there was an advantage to making donations. You also received greater opportunities to earn and invest. Finally you increased your likelihood of passing over ‘downsized’ squares which meant you lost money and turns. The underlying lesson was that you ultimately received rewards for giving. I’m not saying that you should give strictly to get, but in our financial system the government does allow you to write off gifts to certain entities and thus lowering your tax.

“Did you get your taxes done yet? Did you get your taxes done yet? Did you get your taxes done yet?” That’s all I heard the first tax season I moved in with Dad just after finishing graduate school. He literally walked through the house asking me if I had done my taxes. I didn’t know why he cared so much, but it started to scare me. Just finishing my doctoral training, a period in which I didn’t have much money, I owed the IRS tax money that year. For those unfamiliar with the process, we had to pay estimated taxes on our $17,000 to $22,000 graduate stipends every year. So yes, the poor do pay taxes too.

Reducing Your Taxes

“I like to make gifts to things that are tax deductible!” One day we were at Dad’s desk, and he had a pile of solicitations from his alma mater and other charities. He made his poignant declaration as he pondered them. He prepared his tax returns himself at that time and it was quite the ritual every year as I observed him.

In hindsight, Dad was probably also feeling some anxiety himself. He lived in one of the highest taxed states in the country – New York. He also owned his home outright and probably wasn’t going to get much in way of homeowner related deductions. In other words, he was likely going to have to make payments to the federal and state governments.

This explains his preoccupation at that time with tax deductible gifts. Unfortunately, I don’t remember the exact verbiage, but we did have a talk about making charitable gifts to certain entities and lowering your tax payment. It was my first time learning these lessons and I was in my late 20s. I know that my mother put money into church in my younger years, but we never talked about the gifts being tax deductible.

Where Can You Make Tax Deductible Gifts?

Well, I just named a big one which will make a lot of people bristle in our increasingly secular society, church. Whether you want to admit it or not, churches are businesses, some bigger than others. Some also do more good than others. Not all pastors, for example, take the tithes and offerings to the church to buy expensive suits, fleets of fancy cars and private jets. Some churches actually use the money raised for missionary activities and helping the poor.

That said, if you belong to a church and give regularly, you will have the opportunity to deduct at least a portion of that money from your tax liability, regardless of what the pastor and the church do with it once you drop it in the plate or donate online. This also explained why Dad kept giving tithes and offerings to his church even when he stopped physically attending. Each week he dutifully wrote his check and put in the church’s envelope with the same smiley face on it. That smiley face always made me laugh. I or my then stepmother, would take it to the church on his behalf.

If you don’t attend church, what about making donations your alma mater? My alma maters are Johnson C. Smith University and the University of Michigan. Many people make generous donations to their alma maters every year. It’s the consistent donations from alumni that ensure that their alma maters maintain solid futures.

Other institutions experience anemic alumni giving and are not so fortunate, causing them to face a loss of accreditation and/or closure. The Historically Black Colleges and Universities are a good example of this. There are also scholarship funds like the United Negro College Fund. Furthermore, throughout the year and around the major holidays, there are regularly solicitations to feed the hungry, especially around the Thanksgiving and Christmas holidays. When watching TV and now online, there are opportunities to give for pretty much any cause around the world whether it be feeding hungry people, or relief from wars.

Again, giving is a wealth-building and maintenance strategy for certain demographics. Come election time, the wealthy regularly get demonized for not paying their ‘fair share’ of taxes relative to the middle and lower classes. I would once again point readers back to the above-mentioned book Cooperation and Coercion for a more substantive discussion of the validity of these claims. I’ll end this point by stating that the charitable giving and philanthropy these high net worth demographics make isn’t highlighted as much (or enough).

Giving Is A Personal Choice

There are several contexts for giving and generosity. It’s something I’ve had to conceptually piece together over my lifetime. My parents helped. The Rich Dad Poor Dad books helped. Dave Ramsey and his Financial Peace University curriculum helped. Life experiences have contributed as well. It’s been a process.

After finishing school and launching off into the adult world of work, one quickly learns that at any given time there can be multiple financial concerns and considerations pulling at you depending on your lifestyle. Perhaps you don’t earn that much money. Perhaps you’re just starting your career and live in an expensive metropolis. Perhaps you have a large student loan payment or are encumbered with some other massive debt. Perhaps your family is dependent on you as the breadwinner, and not just in the context of a nuclear family. In any case, sometimes you might have your hands full just getting your own financial house in order, and you don’t have money available to give.

It may not make sense to willingly give money away. I think the underlying principle in this world, though, is that when you bless others, you get blessed. As my mother often says, “It’s in the Bible,” and there are numerous scriptures which discuss this such as Proverbs 11:24-26 (Give freely and become more wealthy; be stingy and lose everything. The generous will prosper; those who refresh others will themselves refreshed. People curse those who hoard their grain, but they bless the one who sells in time of need.) If you’re not into biblical scripture, just know that under our current progressive tax code as described above, the Internal Revenue Service (IRS) allows you to deduct monetary gifts to nonprofit entities from your tax liability. And finally, there are advantages to paying fewer taxes or none at all.

Closing Thoughts On Tax Deductible Gifts

Thank you for reading this piece. I didn’t write this narrative to tell anyone how to give as everyone’s life is unique. Furthermore, I am not a financial professional, and I am not rendering advice. My intent is to present the information and let the reader decide. This story was rooted in one of many memorable experiences with my father, a retired educator, and it just so happens that I’m publishing it around Father’s Day 2022. Here on the Big Words Blog Site, most of the content published these days is from customers by way of shorter, informational pieces. As the owner of the site I like to publish something of my own from time to time. I started writing this piece months ago, and with the many other things I have to do, I was only able to finish it now.

Author’s Thoughts/Reflections

Tax deductible gifts are a really big deal, and many people give with their tax liabilities in mind. I’m recalling a couple of our Johnson C. Smith University Washington DC Alumni Chapter meetings where members wondered how their gifts to the school would be handled in terms of tax, if they were given through the chapter itself instead of independently.

We often learn a lot from our parents through observation. Many of the life lessons from my father have been money-related. Many of those lessons have involved being very careful with it which can be a strength in some contexts, while it can be a source of conflict and ire in others. As with most things in life, I’ve learned a balance is good and optimal.

The Big Words LLC Newsletter

For the next phase of my writing journey, I’ve started a monthly newsletter for my writing and video content creation company, the Big Words LLC. In it I plan to share inspirational words, pieces from this blog and my first blog, and select videos from my four YouTube channels. Finally, I will share updates for my book project The Engineers: A Western New York Basketball Story. Your personal information and privacy will be protected. Click this link and register using the sign-up button at the bottom of the announcement. Regards.

As many of my readers and YouTube subscribers know, here on the Big Words Blog Site, most of the content published is now coming from collaborators and customers in the form of shorter informational pieces. With multiple YouTube channels and now another blog for more literary writing, I only have time to write and publish a few pieces of my own here. While others opted for the Moderna and Pfizer vaccines, I took the Johnson and Johnson Covid-19 vaccine within the last month and as a scientist, I wanted to write something about it.

As described in my initial submission on the new ScoonTV publication, one of the videos on my science and technology YouTube channel was taken down for ‘violating community guidelines’. I have since been hesitant to talk about the vaccines in any way, but with this platform belonging to me, I can discuss whatever I want to. Whether or not the social media platforms allow it to be shared, remains to be seen.

As you know there was a lot of controversy surrounding the Covid-19 vaccines, in addition to the pandemic itself. When talking with a good friend, I pondered that the pandemic may have been the younger generations’ World War 2 or Vietnam, in addition to maybe the 911 attacks. That is no disrespect to anyone who lived through those wars and tragedies or participated in them, but none of the younger generations have lived through a crisis like this.

My Reasons For Getting Vaccinated

I decided to take one of the Covid-19 vaccines for a number for reasons. As described, for a period I uploaded several videos on the pandemic on my science and technology YouTube channel. In short, I honestly was not one of the individuals who was in a rush to get vaccinated. In my opinion there were some very peculiar circumstances surrounding the pandemic which I will not go into here, but to some degree, the need to vaccinate everyone did raise my antennae along with those of other people. In short, I wasn’t going to be one of the first to get vaccinated and took a “wait and see approach”.

In that regard, seeing my relatives get vaccinated with no adverse reactions helped allay some of my concerns. Other individuals who were close to me received their vaccinations was also another line of evidence for me. Ultimately, like most everyone else, I wanted to be able to move about freely without concern and get back to a level of normalcy.

Returning To Normalcy

On that same vein, the featured image for this story is from my trip to the Albany area for Father’s Day 2021. Prior to the pandemic, I made two to three trips a year to New York State’s Capital Region to visit my father via train. During the pandemic, I defaulted to making the five-hour drive to the Albany area and the eight-hour drive to Buffalo to see family. Needless to say, that driving is more work than simply closing one’s eyes, or looking out of the window and daydreaming on a train or an airplane.

Going back to the featured image, it was taken trackside next to my Northeast Regional Train in Alexandria, VA. Amtrak did not mandate its passengers to be vaccinated, though we did have to wear masks once boarded, a rule that was respected by some and not by others. The first leg of my trip from Washington, DC to the New York City area got a little more crowded than I was comfortable with. The second leg from New York City to Albany was relatively empty though. The same was true for the return trip.

What’s In The Three Vaccines?

Now in terms of the vaccines themselves, having backgrounds in Pharmacology and Toxicology, my focus was always on what was in the vaccines in terms of ingredients (active and inert). I wanted to get a feel for their “pharmacodynamics” and potential side effects. In today’s information age, there were lots and lots of rumors and theories floating around about nanotubes and microchips being injected into us. My mother told me that someone in her circle believed that the vaccines would ‘magnetize’ our bodies. It was like the hysteria surrounding 5G technology when people attempted to make it the cause of the pandemic.

While many people are skeptical about the work done of the Food and Drug Administration (FDA), their mission from the regulatory context is to protect the health of the nation and to make sure that the foods and medications we take are safe. The vaccines thus had to go through the FDA for approval for “emergency” usage. To determine the safety of the vaccines, I pulled the memoranda for each of the three vaccines approved in the United States from the FDA’s website to ascertain what was in the vaccines.

The following are the ingredients contained in the vaccines. The verbiage and characterization were lifted directly from the FDA memoranda which are hyperlinked in case readers want to go and look for themselves. The “efficacy” and side effects are also characterized in each memorandum.

The Moderna Vaccine

The Moderna vaccine is an off-white, sterile, preservative-free frozen suspension for intramuscular injection. The vaccine contains a synthetic messenger ribonucleic acid (mRNA) encoding the pre-fusion stabilized spike glycoprotein (S) of SARS-CoV-2 virus. The vaccine also contains the following ingredients: lipids (SM-102, 1,2-dimyristoyl-rac-glycero- 3-methoxypolyethylene glycol-2000 [PEG2000-DMG], cholesterol, and 1, 2-distearoyl-sn-hocholine [DSPC]), tromethamine, tromethamine hydrochloride, acetic acid, sodium acetate, and sucrose.

The Pfizer Vaccine

The Pfizer-BioNTech COVID-19 Vaccine is a white to off-white, sterile, preservative-free, frozen suspension for intramuscular injection. The vaccine contains a nucleoside-modified messenger RNA (modRNA) encoding the viral spike glycoprotein (S) of SARS-CoV-2. The vaccine also includes the following ingredients: lipids ((4-hydroxybutyl)azanediyl)bis(hexane-6,1-diyl)bis(2- hexyldecanoate), 2-[(polyethylene glycol)-2000]-N,N-ditetradecylacetamide, 1,2-distearoyl-sn- glycero-3-phosphocholine, and cholesterol), potassium chloride, monobasic potassium phosphate, sodium chloride, dibasic sodium phosphate dihydrate, and sucrose.

The Johnson And Johnson Vaccine

The Janssen COVID-19 vaccine is a colorless to slightly yellow, clear to very opalescent sterile suspension for intramuscular injection. The vaccine consists of a replication-incompetent recombinant adenovirus type 26 (Ad26) vector expressing the SARS-CoV-2 spike (S) protein in a stabilized conformation. The vaccine also contains the following inactive ingredients: citric acid monohydrate, trisodium citrate dihydrate, ethanol, 2-hydroxypropyl-β-cyclodextrin (HBCD), polysorbate 80, sodium chloride.

Getting My Shot

Assuming none of the ingredients were intentionally omitted, nothing I read personally in any of the vaccines alarmed me. I chose the Johnson and Johnson vaccine because I liked the mechanism of action more (a DNA Adenovirus vs micro RNA), and I just wanted to take one shot and be done with it. I was discouraged, though, after the Johnson and Johnson vaccine was initially pulled for a rare side effect, blood clots, I believe. When I decided to get vaccinated, I could not find it initially and then one day when doing a random search online, I saw that the CVS pharmacy that I frequent at Pentagon City was, in fact, offering it. After making a reservation, I went and got it on a Friday around noon.

I was cautioned from the nurse or pharmacist that I might experience symptoms of some sort over the next 48 hours. There was the inevitable pinch/sting from the needle and then I felt a sensation in my shoulder which radiated up towards my neck. That went away quickly. I hung around in the pharmacy area for the next 15-20 minutes as instructed. I then took my complimentary 20% off coupon, purchased something and left the store. I did not expect any adverse reaction(s) as I keep myself healthy and have faithfully taken vitamins C, D, E and Magnesium since the pandemic started.

Abandoning Our Masks?

And that was my vaccine experience. I did not write this to sway anyone. Again, as a member of the science community, I just wanted to share my story. I am happy that I got the vaccine I wanted, though I saw an article on Yahoo that said that the Johnson and Johnson vaccine has not rebounded from the initial pulling in terms of popularity. I do not know if this means that it will be abandoned altogether, but I hope not, especially if it has efficacy against the new “Delta Variant”.

I have not completely abandoned my masks. I honestly will have to get used to not using them again. As described earlier, Amtrak insisted on its passengers using them and at least initially and when I fly, I am certain the airlines will also err on the side of caution. For the type of mask I had, it was not that bad for the seven hour ride.

Some stores and proprietorships are still mandating mask. Interestingly, before making my Father’s Day trip, New York State, one of the most vigilant of all the states during the pandemic, lifted all its restrictions. I met up with some old friends at Latin Dance Night in Albany, and no one wore masks as they danced up a storm, respired all over the place and socialized that night.

Do you have a vaccine story? Please feel to leave some comments below this piece. Also please subscribe to my science and technology YouTube channel to hear more science-related discussions like this. I am about 225 subscribers away from the holy number of 1,000.

As many of you know, I’ve branched out from the Big Words Blog Site into YouTube where I now have four channels. My original channel is Big Discussions76 where I now discuss general topics. One of my recent guests is fellow Buffalonian Dennis Wilson Jr. (see the video at the bottom of this post). Being in the same peer group, Dennis and I played basketball in Buffalo’s “Yale Cup” high school basketball league around the same time in the early 1990s. After launching a career in education, Dennis started and has steadily built his own business empire. In addition to owning one of the more popular restaurants in Buffalo, the Oakk Room, Dennis further hosts high quality and sophisticated events and has also started his own clothing line.

In this interview, I asked Dennis about his background, his educational path, how he launched in the business world, and finally what he foresees going forward. Links to Dennis’ business websites are in the description box below the video. If you want to read more about business topics of all kinds including branding, select the “Business/Entrepreneurship” category from the list of topics in the drop-down menu in the left-hand margin my blogging platform. Thank you for watching, and if anything in our discussion resonates with you, please like, share and subscribe to my channel.

“I personally recommend having a year’s worth of savings in the bank!”

Note. Like my Net Worth piece, the subject matter of this blog post is not new. It has been known for years by those who’ve learned about it in their families, learned about its concepts in business school, or have discovered it on their own. It’s a discussion from my personal perspective which I think is worth visiting. Also, while this is a ‘money’ topic, I’m discussing it from a ‘scholarly’ perspective. I’m not rendering financial advice where I’m telling readers what they should do. In the spirit of the first principle of my blog, Creating Ecosystems of Success, I’m simply introducing a concept and discussing why it’s important for the lay person; so they can make their own life choices.

* * *

Reflecting on my youth, both of my parents were savers and they showed that in their own unique ways. As described in my piece regarding budgeting, my Auntie Adele was quite the budgeter and she was always outspoken (and vigilant) about that. All of the pieces were there in my mental periphery, though it wouldn’t be until my adult years that I’d figure out how every piece in terms of one’s personal finances ‘fit together’ as I’ll describe later. I’ve learned that you can hear about something, but it’s not until doing it yourself that you actually understand it. This is why Rich Dad Poor Dad author, Robert Kiyosaki, frequently referenced the “Cone of Learning” in his books.

Though I intuitively knew what ‘emergency funds’ were before taking Dave Ramsey’s “Financial Peace University (FPU)“, I got a much clearer picture of what they were and why they’re important. I’ve covered many other important aspects of personal finance here on my blogging platform, but after a potential collaborator emailed me recently about linking their online resources to some of my content, I realized that I never covered emergency funds. It’s a topic that is timeless in terms of importance and is especially relevant with my recently purchasing a new car. As such, I think I’ll use that a jumping off point for this piece.

If you don’t know, I’m a YouTube content creator now and have four channels. My original Big Discussions76 channel now covers several topics, financial literacy/money being chief among them. I recently shot a video discussing my decision to acquire a vehicle after going without one for eight years. You can watch that video in the link below. If you do, please kindly give a like, share it in your network and subscribe to my channel.

I also wrote two pieces discussing why I decided to go without car ownership. In those pieces and in my YouTube video, I communicate that one of the checked boxes for rejoining the car ownership club was having a fully funded emergency fund. In FPU, Dave Ramsey describes a fully funded emergency fund as one that contains three to six months of savings based upon the critical items on your personal budget. That’s actually a little more on the liberal side. Some people, like one of my mentors, are more conservative and believe that one (or a couple) should have a year’s worth of savings in the bank! If your personal finances are highly leveraged credit-wise and you’re living paycheck to paycheck, this may all sound like a gargantuan task, but from personal experience, I can assure you that it can be done.

I can’t lie though, in that it does take a great deal of determination, grit, and delayed gratification to create a fully funded emergency fund. Spiritual folks would also say that it takes a great deal prayer. In either case, you must know what your ‘why’ is, or your motivation. That will help keep you going even when things feel lonely or even get hard. What was my motivation for creating an emergency fund? Let us go back to car ownership.

“Cars are built to breakdown,” said Mr. Cholley Gray of the former Gray’s Auto in my hometown of Buffalo, NY. In my trips back to Buffalo from Charlotte, NC, Mr. Gray performed most of the repairs on my first car, a white 1990 Subaru Legacy which was passed down from my mother to my brother, and then to me. Having been through seven long years of Buffalo winters, I inherited the car right around the time when rust started taking hold of many of its parts and wear and tear had set in. I went through numerous transaxles when I owned that car. Each was $150-$200 each time.

The biggest and probably the costliest repair was the “rack and pinion” which went out on me down in Charlotte, NC. For those unfamiliar with the inner workings of automobiles, the rack and pinion is a part of the power steering system. When the piping rusted out that fateful day, the car became extremely difficult to steer and it made what I would call a howling or a screeching sound like a saw cutting through wood. One of my professors and I investigated the systems of the car in his driveway and saw that it was literally bleeding the pink power steering fluid. It was a fixable repair, which came at a price of $850. As an undergraduate I was mortified by the price in addition to the sound the car was making. Fortunately, my father was there to send me the money, just as he was there to purchase the car for me from my brother and pay for my insurance.

My burgundy 1996 Saturn SL2, which I purchased in Ann Arbor, Michigan while in graduate school, had two costly repairs within the final six months of grad school. This led me to bow out of the car ownership club in the summer of 2012. One night near my job, one of the front wheels rusted out completely. That is the entire support stabilizing the wheel needed to be replaced. That costed $1,200 at Meineke which was my entire federal income tax return that year. Only months later, the cable attached to the manual transmission broke while I was driving. Fortunately, I wasn’t on the expressway and was able to pull off onto a side street without being harmed. That repair also came out at $1,200 which was the final straw for me. Mentally, I’d already prepared for getting rid of the car, like a loved one on life support.

Probably the most painful repair though, was around 2010 when the radiator cracked in the scorching Northern Virginia summer heat. Not only was that repair $500, but the mechanic, an Asian guy named Steve, bitched at me and jeered me about getting a new car when I picked it up. The nerve of that guy, right? After all, I paid him for his service. My girlfriend at that time pretty much agreed with him on the spot, making a bitter afternoon more bitter. At that time, I was temporarily living with her while closing on my condo unit. I planned to give her something for that month towards the rent, but because of the transmission going out, I couldn’t pay her, which she secretly held against me and sprung it on me during one of our many future arguments.

If it sounds petty for me to tell this side story about my ex, rest assured knowing that there’s a grander purpose. Sometimes in life we set out with good intentions and unexpected things happen affecting the entire mosaic. If we’re not prepared, domino effects can result making situations exponentially worse. I’m saying all of this to say that life is so much better when you have an emergency fund, a stash of money saved just in case something goes bad. It literally gives you peace of mind. Everything is just different because you’re not constantly worrying about something going wrong or breaking. When something does break, wears out, or needs to be replaced, you’re not scrambling for money or to take out loans. It’s truly a different way of living. “Murphy leaves you alone,” as Dave Ramsey jokingly says.

Having an emergency fund also allows you to potentially help those around you. Going back to the girlfriend described above, there was another instance where she needed to get new tires on her car to pass the state inspection. By the way, she was educated and had a career of her own. That said, I was still expected to take care of her in certain ways. This is a prevalent expectation and I’m not disputing it as I understand the psychology of it more now. It’s just something for some men reading this to be cognizant of. There is more I could say about it, but that’s a separate discussion.

At that time, I didn’t have a fully funded emergency fund and was unable to safely pull the $300-$400 out of my savings to pay for her new tires. I’ve often wondered if she would have been more ‘human’ to me throughout that relationship if I could have done more for her financially. Based upon what I know now, the answer is yes.

Going back to when I discussed ‘safely’ pulling the money out of my savings, let me unpack that a little bit more. A decision you must make when someone comes to you for help, or announces that they’re in distress, is whether or not you can afford to help them. Put another way, will you potentially later need the money said person is asking you for? If so, you may not be able to help them because if you do, you may be stuck asking someone else for help later on yourself, another domino effect.

The other thing is that after being both the lender and lendee, I agree wholeheartedly with Dave Ramsey in terms of loaning money. I don’t believe in loaning money anymore. If someone comes to me these days for help, I assess whether or not I have the money to give. If I can’t give the full amount, I give what I can and don’t expect anything back, as loans put a mutual strain on personal relationships. From a spiritual standpoint, Proverbs 22:7 reads, “The rich rule over the poor and the borrower is slave to the lender.” It’s something for everyone to ponder, especially with friends and relatives.

I’m going to close with two more points. The first of which is that while I discussed emergency funds in the context of automobile ownership in this piece, it reaches into many other areas. In the last five years, I’ve lost a cell phone, I’ve had to replace my refrigerator, and the toilet in my home.

I’ve also refinanced my mortgage a couple of times. While not an emergency per se, these have involved me using some of my savings to help the transactions go through. Speaking of savings and mortgages, if you can’t purchase your home outright with cash, one of the key things lenders will be looking for when deciding to qualify you for a mortgage, is your history of saving money. Likewise, the more you have saved, the better the loan terms you’ll get if you qualify. I’ll also jokingly state here that me and the ex-girlfriend discussed above got into a standoff over this point one night. My father and I had also talked about this before. I was factually right, but sometimes being right in relationships just causes more drama and resentment.

My final point involves retirements savings. Some individuals have started saving in their retirement accounts which is absolutely the right thing to do as employees. Unfortunately, when adverse events occur, some people must use credit cards, loans or raid their retirement savings because they don’t have any other ‘liquid’ cash available. Raiding your retirement savings involves a tax penalty and unplugs the money from ‘compounding’. An emergency fund thus provides a layer of protection for your retirement nest egg, and that’s an important though not widely understood reality about retirement savings.

With all of this being said, a fully funded emergency fund, while an important piece of your financial health, isn’t an ultimate layer of protection. There may be bigger adverse financial events looming and that’s what your insurances are for (health, car, homeowner, renters, etc.). That’s a separate topic all in itself, but one that everyone should also consider.

• They improve your overall peace of mind, health and quality of life just by relieving financial stress. • They allow you to absorb and recover from negative financial events (but also remember that insurances are important). • They protect your other savings and investments and allow you to easily navigate transactions like home purchases and refinances. • They allow you help those around you (if you can afford to).

In closing, keep in mind that your emergency fund is not meant to be the investment of the century, just a layer of protection against life, and it acts as insurance in a way. Though it may be sitting in a savings account not making much interest, you want to be able to get to it quickly in case of an emergency (not for frivolous spending). There are savings accounts that can earn more money for you such as a money market account, but again that is not the main point of all this. The point is to protect you and your investments.

Thank you for taking the time to read this post. As of now I’ve written several financial pieces on my blogging platform and many of them are listed on the bottom of the Big Word Blog Site’s home page. I’ve also published numerous shorter money and business-related pieces with guests and contributing writers. You can find those by simply searching my categories menu on the home page or by typing “money”, “finance” or “business” into the search box at the bottom of the home page. If you read something you like, please leave a comment and share in your network via email or in your preferred social media space.

To receive all of the most up to date content from the Big Words Blog Site, subscribe using the subscription box in the right-hand column in this post and throughout the site, or by adding the link to my RSS feed to your feedreader. Please check out any of my four Big Discussions76 YouTube channels. Lastly, follow me on Twitter at @BWArePowerful, on Instagram at @anwaryusef76, and at the Big Words Blog Site Facebook page. While my main areas of focus are Education, STEM and Financial Literacy, there are other blogs/sites I endorse which can be found on that particular page of my site.

Before I start this story, I want to issue a warning to the ‘low attention span’ people. This post is roughly 2000 words. Thus, if you can’t focus for that long, feel free to leave now go and read something else. I can assure you though that this is a fun and educational story with some very important points at the end. With that, I’m going to jump in.

Another Dad Story

Well it’s that time of year again, Father’s Day. As such, just as I have prepared a 2020 post for Mother’s Day, I have also prepared a 2020 post for Father’s Day. Like my first ever Father’s Day post on my blogging platform, this story involves a subject that’s near and dear to my heart, money and wealth building. As with all my Dad stories, this one made a lasting impression on me as I hope that this does for any readers.

In his prime and slightly beyond, my Dad was a force to be reckoned with, one which struck fear into me, even in my early 30s. I lived with him in New York State’s Capital Region during my postdoctoral fellowship which turned out to be an educational experience on several different levels. It was a surreal two and a half years in hindsight that forever changed me. Some of the changes were due to external factors while some were due to internal factors.

Lessons from Rich Dad

Just before leaving Ann Arbor, MI for the Albany area, I picked up Robert Kiyosaki’s Rich Dad Poor Dad book and discovered the worlds of financial literacy and wealth building, worlds I didn’t know anything about at that time. Most of my life I had my eyes set on being an employee. Reading about being and an investor and all the concepts associated with it was exciting though. According to Kiyosaki, there were people becoming wealthy not by slogging off to work everyday and punching a clock, but instead by acquiring financial asset investments.

In addition to Kiyosaki’s books, I purchased a copy of his game, Cashflow 101, the electronic version. Unlike the board game version which you have to play with other people, I could sit down at my PC and play every night. The goal of the game is to get out of the Rat Race and onto the Fast Track. For those who have never played the game, you must choose a profession. The chosen profession comes with a salary, and a certain number of assets and liabilities. The cost per child varies with profession as well.

A Lifelike Game

The game is realistic in that high income professionals like doctors, lawyers and airline pilots make more money than the janitors or the web designers. They also have greater expenses and usually more student loans in the case of the doctor and lawyer. They might even have loans under debt review as a result.

Take a look at my 2018 Father’s Day blog post which has a special significance for my brother, my father and me. That post coincidentally involved careers in medicine and law which Dad wanted my brother and me to pursue. Going back to the game, individuals playing the game must figure out how to generate enough passive income from their investments to pay all of their bills monthly and annually. This allows them to become financially free and moves them onto the Fast Track, and live the life of wealthy business owners and investors.

On the road to getting out of the Rat Race, in addition to getting the opportunities to participate in stock and real estate deals, participants sometimes also have children, have to purchase doodads (random expenses or luxuries which drain your money), and face unexpected crises like car accidents, all of which can act as financial setbacks. This forces players to think about their objectives creatively and still figure out ways to get out of the Rat Race. In terms of the game, I’ll stop there. It’s an intoxicating game, and it’s one that I highly recommend. Suffice it to say for now, that as I played and started learning, I started experiencing a paradigm shift and aspired to do the same things in real life, things that I would later find were easier said than done. By the way, Dad saw me regularly playing the game and probably thought I was nuts.

Real Estate Investing and Taking Action

One of the things Robert Kiyosaki discussed in Rich Dad Poor Dadwas real estate investing and I became interested in it. Some friends of mine in the area were also interested in it and turned me onto our local real estate investing club which I won’t name. There were monthly meetings where the President encouraged us to get into deals and to, “take action.” There were also big time real estate speakers like the land lording guru Don Beck, whose program involved putting your rental properties on ‘cruise control’ and also creating rental leases that were as protective as possible for the land lords against the problem tenants.

Most of the club members were seniors in terms of age and my two friends and I may have been the only minorities there. Coincidentally an older woman, named Mary, agreed to mentor me. Mary had been in the game for a while and had already started acquiring properties. I think she had her Multiple Listing Service (MLS) certification and had the ability to search its databases. I met another younger guy, whom I’ll call Tyler, who also had the wealth-building mindset and was living it. We talked one Saturday during a field trip we took around our area to look at properties. Tyler turned me on to T. Harv Ecker’s book, Secrets of The Millionaire Mind, which is a short but good read.

Like our President, Mary also encouraged me to do my first deal and we started looking at properties in the Albany area. I recall once going into an empty brownstone and looking around with her near the Albany state capital where my research lab was located. We eventually found a duplex in the downtown area, with a flat roof and one tenant living in it already. Mary suggested that I could live in one unit for a little and rent the other unit out (owner occupied status). Eventually I could move out and ‘cash flow’ the entire property. It all sounded cool and a little scary. I wanted to do it, but how would I do such a thing?

Early Lessons in Real Estate Investing

For those unfamiliar with purchasing real estate, there are usually three critical items lenders want to see: employment history of some sort (especially if you’re new), your credit score and savings of some kind (over a series of months, not random gifts). Depending how savvy you are, you may be able to structure your deal so that you don’t have to pay the closing costs up front. I just barely qualified in terms of my credit score. It wasn’t great at the time, but it was just good enough. I’d only finished my Ph.D. one to two years earlier. I paid my bills on time, but I was over-leveraged credit-wise for numerous reasons which I won’t discuss here. Finally, I had $2,000 to $3,000 in the bank, but I knew that I would need more. Where would I get it from though? Enter Dad!

Now before I go on, let me warn you that this part of the story gets a little painful, but exciting at the same time. I could save this detail until the end, but it’s worth pointing out here. One of the things this experience (and others) taught me going forward was that while we are all physically living on this world together, we can all exist in different worlds and have different world views. Science is a world of its own. Salsa dancing is a world of its own. Writing is a world of its own. Real estate investing is a world of its own. Being an employee is a world of its own. Each world has its own unique set of rules and mindsets.

Dad gets Involved

Dad was an employee and an excellent at budgeting and saving. He was also risk averse money-wise, and he had his own personal real estate experience that turned him against land lording forever. According to Dad, he once had a tenant in his lower unit, an older woman. According to Dad, he went downstairs to collect the rent one day, and the woman slid into a supernatural trance where her eyes rolled back and her ears pointed upwards. From that point on Dad never wanted anything else to do with real estate investing and land lording, no matter what the upside was.

I don’t know whether Mary suggested it, or by default I decided to ask him for a loan, but after much internal deliberation, I did and that’s when things got, how shall I say, exciting. I knew my father and lacked confidence when asking him for the financial help. I was pretty scared actually. He didn’t say no immediately, but instead looked at me with a blank stare and told me he’d think about it. I intuitively knew that instead of simple yes or no, it was going to turn into a long drawn out process, and Dad didn’t disappoint.

Dad Weighs In

Dad did, in fact, think about it. His thinking stretched from days to weeks which for me was like death by a thousand cuts as one of my favorite YouTube content creators often says. He asked me questions about my investment idea often from the other room when I least expected them. In some instances, we were in the same room and he’d ask me questions about it with his back to me with no eye contact. Yes, I know it’s odd, but it was just how he communicated with me at the time. At some point I told him to just forget about it, but it continued.

“How much money do you have in the bank?” I don’t remember when in this ordeal that he asked me this question, but I just remember that he asked it. The question suddenly made me feel defensive, naked, picked over and violated. “The bank will want to know how much money you have!” Dad was right about this as I found out in the future when applying for mortgages and refinancing on my own. I actually uttered these same words in a money-related dispute with an ex-girlfriend; that didn’t go over well, by the way, so be careful in those instances.

“I have $2,000 to $3,000 in my savings and my Self-Directed Roth IRA,” I pensively replied.

$2,000 to $3,000 is NOT Money!

“That’s NOT money!” Dad quickly and sharply declared with the precision of an assassin. His words were cutting, and I felt insulted and angry afterwards. I didn’t understand why this whole thing had to drag out like this, and I didn’t understand why we couldn’t just sit down and have a simple step by step discussion about why it wasn’t a good or bad idea. The thing I learned later though was that Dad was right.

What Dad meant by saying that, “$2,000 to $3,000 is NOT money,” was that it wasn’t enough money to safely do what I was thinking about. As in all cases, money is relative. There are people who don’t have $400 saved up and there are people who don’t have $1,000 saved up, so to those people, $2,000 to $3,000 is a lot of money. Speaking of $1,000, losing $1,000 can hurt if you’re not prepared to lose it, which I did when trying to do a real estate deal one to two years after moving to the Washington, DC area.

Some Real Estate Investing Tips

I want to tie up this blog post with my major learning points from this story. They are as follows:

• It’s best to invest safely: Whether you’re investing in real estate, stocks or something else, it’s important to do so from a place of safety. At the time of writing this, to me that means allocating funds strictly for that purpose separately from your essential expenses. This way, if the investment falls through, you’ll still have a place to live, food to eat, clothes on your back, etc. Investing is different from outright gambling, but think about how much more fun a trip to a place like Las Vegas is when you have enough money with which to gamble. Don’t invest your emergency money, the rent or the mortgage. This leads to my next point which involves friends and relatives.

• Be careful about involving the finances of friends and relatives in your business/investing ideas: From 30 plus years of being his son, I knew that Dad was risk-averse and didn’t play around with his money, but his not loaning me the money turned out to be the best thing for both of us because it would’ve poisoned our relationship, potentially beyond healing. I wouldn’t have felt comfortable around him, and it would’ve always been on his mind whenever he thought about me. If you have a money idea, I think the best things is to figure out how to launch it on your own, or until its far enough along for others to see the upside (and benefit for them). This way, if you take the loss, you take it on your own. If you are going to partner with friends or relatives, make sure you share the common vision and that they understand the risks. Finally, I’ve learned that when you’re launching an idea, whether it’s stocks or some other opportunity, savvy investors/partners are more likely to participate in your idea if they can see that you’ve already thought out and invested a significant amount of your own resources into it, unless of course you have an extensive track record of doing what you’re proposing.

• Real estate is a fun and potentially rewarding area, but a complex and dangerous one too: Robert Kiyosaki’s Cashflow 101 is a fun and educational game which to this day I highly recommend. It’s just that thought, a game played with fake money. The game is designed to expand and transform your mindset. Getting out in the field and taking action which most real estate teachers teach, is a different matter. Getting an investment property was a good idea, and Dad admitted that, if I recall correctly. However, not only did I not have enough of my own money in the bank yet, it also wasn’t clear if I was staying in the area.

Levels of Experience

Now let me be clear. Am I saying not to own property out of state? Absolutely not. There are investors who own property in other states or cities, and in some instances other countries. Most of them are experienced though. They have the systems in place to be able to do so, and in some instances, they’re partnering with other experienced and like-minded people.

Think about the martial arts. Dad was a Judo guy so let’s use Judo. The masters in martial arts dojos typically wear the brown and black belts, and one must practice and train hard to reach those levels after starting at the color white. Some trials and errors are involved in ascending to the brown or black belt levels which includes blood, sweat, tears, and being thrown to the mat innumerable times in this case. I would equate this to my lost $1,000 described above which I’ll revisit later on. In short, at the time of my asking Dad for that help, I was the equivalent of a white belt in the real estate dojo.

• Be careful who you share your dreams and aspirations with: Finally, I’ll just say that not everyone is going to understand your dreams and visions, so you can’t share them with everyone. This includes friends and relatives, and this is what Robert Kiyosaki meant towards the end of Rich Dad Poor Dadabout finding new friends. Let me be clear in that this doesn’t mean discarding your old friends. It just means that if people don’t understand the world you’re operating in, have had a negative experience in it, or are just not like-minded in general, they may kill your dream. This goes for significant others and love interests as well. So, for your own sanity, be mindful.

Conclusions

So that’s all I have to say on this matter, and I hope that this was educational for someone. It was a bitter situation to go through at the time, but I can look back and laugh at it now. I can also admit that Dad’s response towards me helped me see things from a new perspective in terms of the world around me regarding personal finances, dating and mating, and finally, when being approached by friends and/or relatives to help them start their own ideas like coffee businesses, for example.

The Big Words LLC Newsletter

For the next phase of my writing journey, I’m starting a monthly newsletter for my writing and video content creation company, the Big Words LLC. In it, I plan to share inspirational words, pieces from this blog and my first blog, and select videos from my four YouTube channels. Finally, I will share updates for my book project The Engineers: A Western New York Basketball Story. Your personal information and privacy will be protected. Click this link and register using the sign-up button at the bottom of the announcement. If there is some issue signing up using the link provided, you can also email me at bwllcnl@gmail.com . Best Regards.

Those of you who have read my content know that I’ve written blog posts for Mother’s Day since starting the Big Words Blog Site. As per usual, the links to my previous Mother’s Day pieces will be shared at the end of this piece. I thought of this piece, while driving back from New York State’s Capital Region as I was recently checking on my father. My Mom is quite cautious and wanted me to shelter in place as much as possible, but following her example, it was important for me to check on my old man during this Coronavirus/Covid-19 Crisis/Pandemic.

Before I get into the messages in this piece which I hope to keep short (by my standards), I want to tell any readers that while our country is looking to reopen shortly, and while infections by the Coronavirus are expected to fall off during the warm weather months, beware of a second wave. It’s predicted that when the cold winter months return, infections will as well. This blog post in some ways may in fact serve as a survival guide for some people who were unprepared for this first tsunami, and it may be helpful should there be future lockdowns and quarantines.

So in terms of Mother’s Day, as I drove back to Washington, DC recently, it occurred to me that my mother imparted some valuable nuggets in my life that helped me survive over the last two months since our country went into this lockdown. Among them are:

• The Ability to Cook: In previous Mother’s Day blog posts, I discussed the home that my mother created for us. A part of that was the meals she prepared for us, ALL of which were prepared with her hands from scratch. Her ability to cook along with my natural curiosity resulted in my ability to cook. I often jokingly tell people that at an early age, I was in the kitchen trying to figure out how she made those scrambled eggs. In addition to picking up recipes of all kinds over the years, from other people and from cookbooks like those from Emeril Lagasse, there are quite a few of Mom’s recipes that I took with me when I left the house. There are secrets that I’m still collecting today, such as most recently how to steam the green beans and onions with enough flavor and succulence at the time of consumption. I’m saying all of this to say that when the lockdown started, I already knew how to cook, so I didn’t severely feel the bite of not being able to eat out. The ability to prepare your own food is a critical skill and if there is in fact a lull in the infections, I would encourage people to learn how to prepare as much of your own food possible. Also learn to prepare healthy foods that you can eat for days at a time and even store for later. That said, I’ve learned that not everyone can eat leftovers, but we learned to do so. Finally, cooking at home also saves you money and stretches your dollars out time-wise.

• Personal Health: In addition to cooking, Mom was big on vitamins and even natural herbs and remedies. Likewise, as I was leaving Buffalo as our country was going deeper into the lockdown, she strongly encouraged me to start regularly taking Vitamin D which has therapeutic benefits for our immune systems. As I’ve been quarantining, I have in fact made Vitamin D a regular part of my daily diet and now Vitamin C as well. I shot videos on my science and technology YouTube channel about the benefits of both vitamins. Please check out those videos and my channel.

• Education, Writing and Building: I give my mother a lot of credit for the blogging platform you’re reading this post on right now. Both parents stressed education at an early age, but it was my mother who insisted that me and my brother learn how word process with proper form at an early age. We also had a computer in the house when we were young, so she saw the wave of the future coming in the early- to mid-1980s. Social distancing and quarantining isn’t natural for human beings and hasn’t always been pleasant at times, but I’ve been fortunate to be able to be keep myself busy and my mind occupied, writing and publishing content. Just as my mother was able to turn her writing abilities into a business, I have as well, which I’ll describe shortly via written content here on the Big Words Blog Site and on my Big Discussions76 YouTube channel.

• The Importance of Faith and Spirituality: Faith and spirituality can be a polarizing topic these days, but no matter how much you have or what you believe, it’s important to have it. Mom was always big on faith. When I go home to Buffalo, I try my best to get myself out of bed on Sunday mornings to attend her church’s services. Just before the lockdown set in, I was at home in Buffalo for two and a half weeks and I attended the last church service at the Mount Olive Baptist Church in Buffalo where the members, like most churches, were able to gather for the last time in a while. Before releasing the congregation, the Pastor read Psalm 91 to us, which was very, very powerful for what was taking place at the time. That scripture is now forever etched into my memory.

So, as I have lots and lots to do, I’m going to stop this here. In the Black community we sometimes dwell on what we didn’t have when we were growing up . We can inevitably get caught looking at what our peers had within our community and in other ethnic groups/cultures. It’s natural in a way, but it’s also important to acknowledge what you were given from your parent or guardian. What did your mother teach that helped you through this challenging time? What might you use if this crisis or another one comes back around?

Oh by the way, fortunately I was able to craft this Mother’s Day blog post pretty quickly and concisely. Right on schedule, Father’s Day is coming up next month and I’ve thought of another really good money-related story involving my father and me which involves a very, very important lesson, so look for it. And in closing, Happy Mother’s Day to all of the mothers out there.

Thank you for reading this blog post. If you enjoyed this one, you might also enjoy:

If you’ve found value here and think it would benefit others, please share it and or leave a comment. To receive all the most up to date content from the Big Words Blog Site, subscribe using the subscription box in the right-hand column in this post and throughout the site. Please visit my YouTube channel entitled, Big Discussions76. Lastly follow me on Twitter at @BWArePowerful, on Instagram at @anwaryusef76, and at the Big Words Blog Site Facebook page. While my main areas of focus are Education, STEM and Financial Literacy, there are other blogs/sites I endorse which can be found on that particular page of my site.

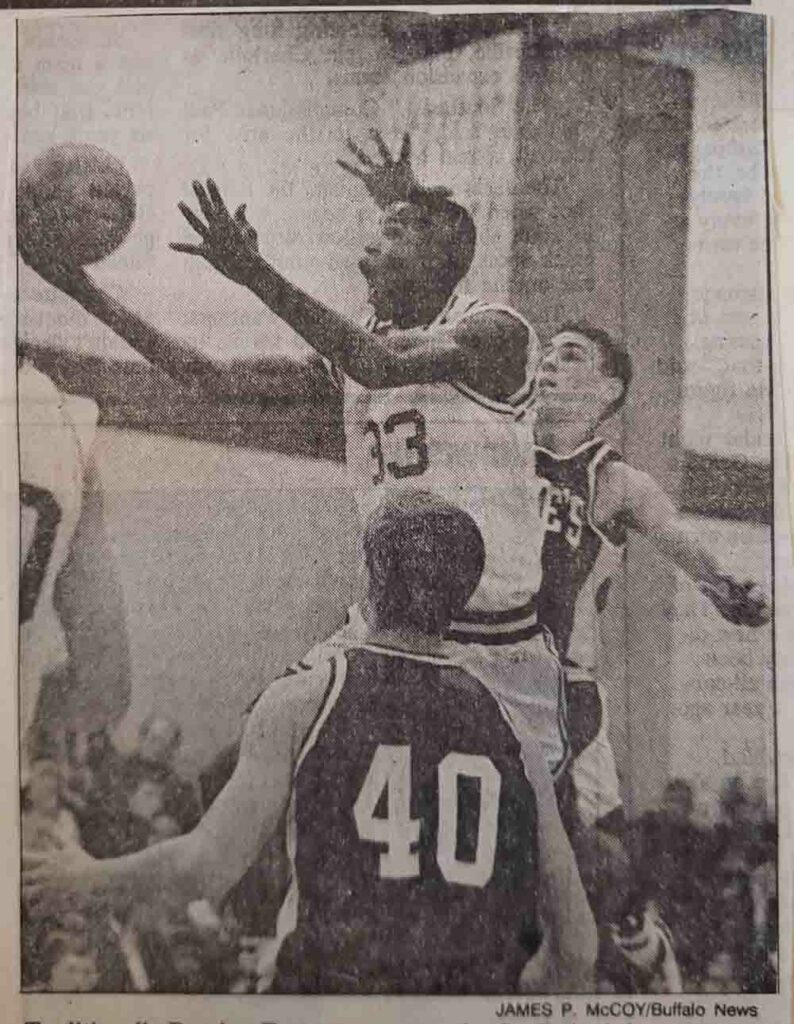

“I think playing in Buffalo alone prepares you for the world, if you’re lucky enough to be able to grow up in the City of Buffalo!”

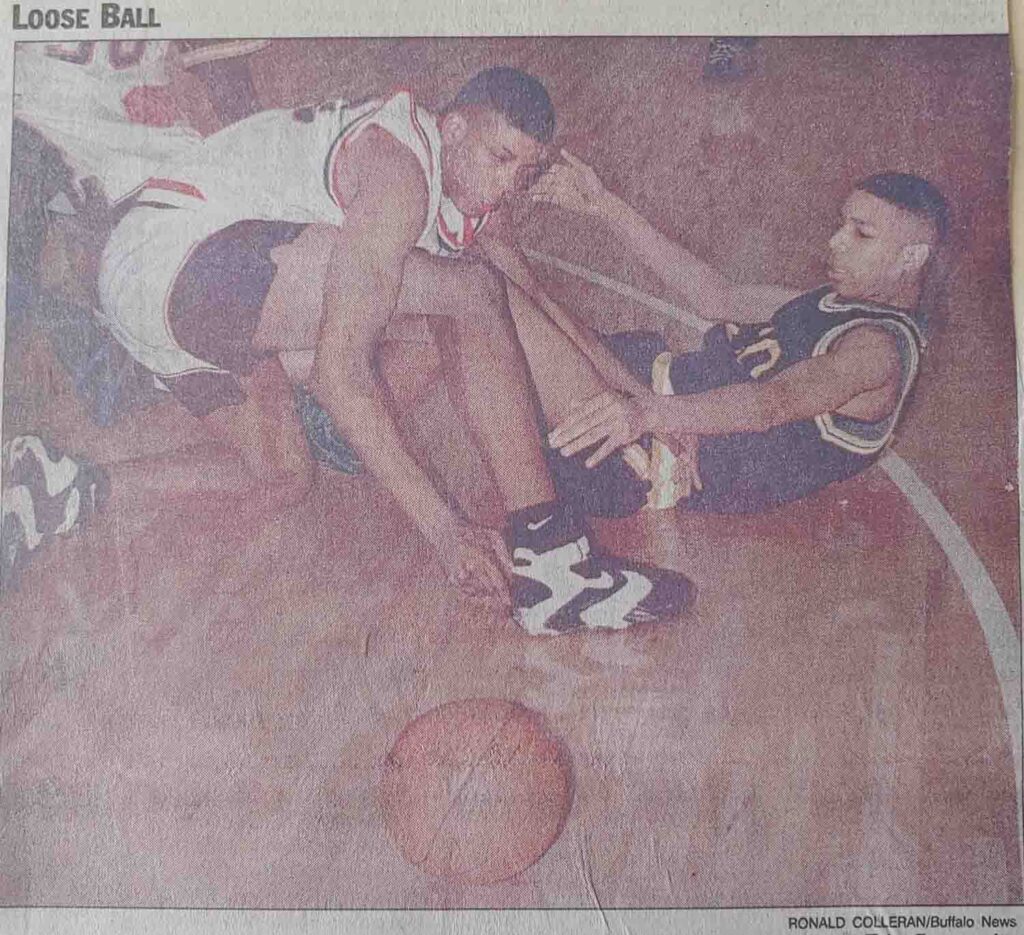

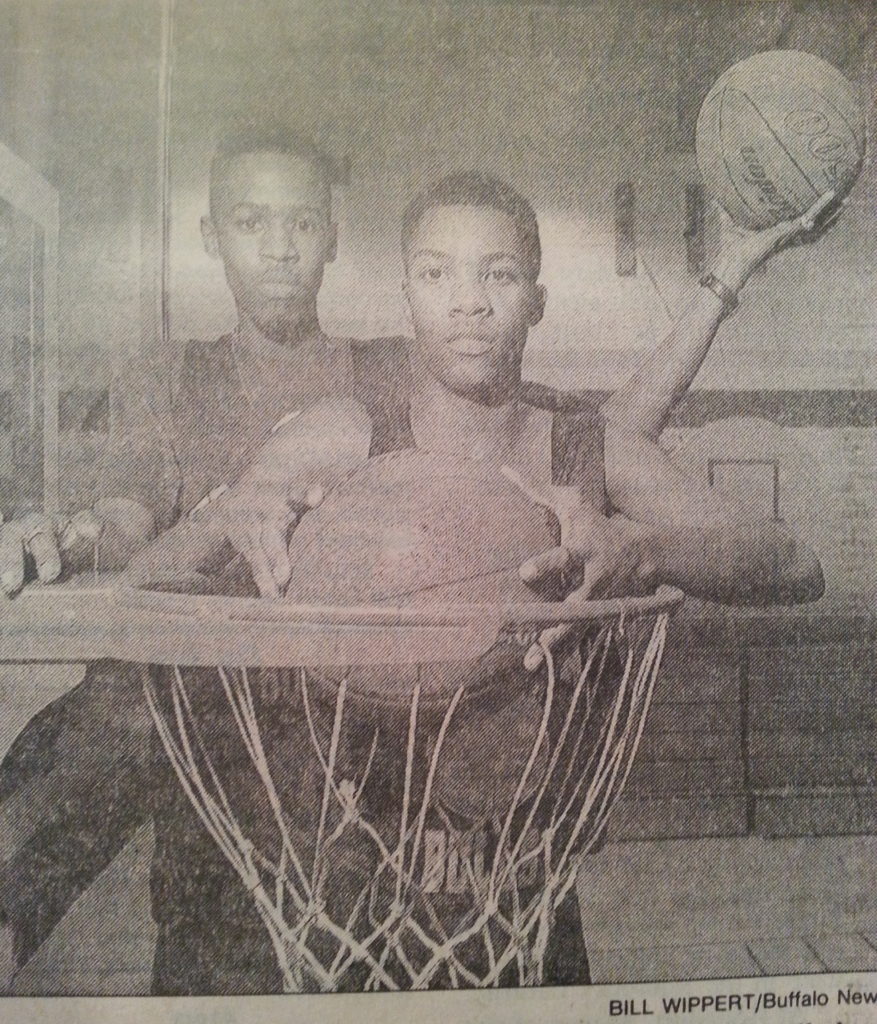

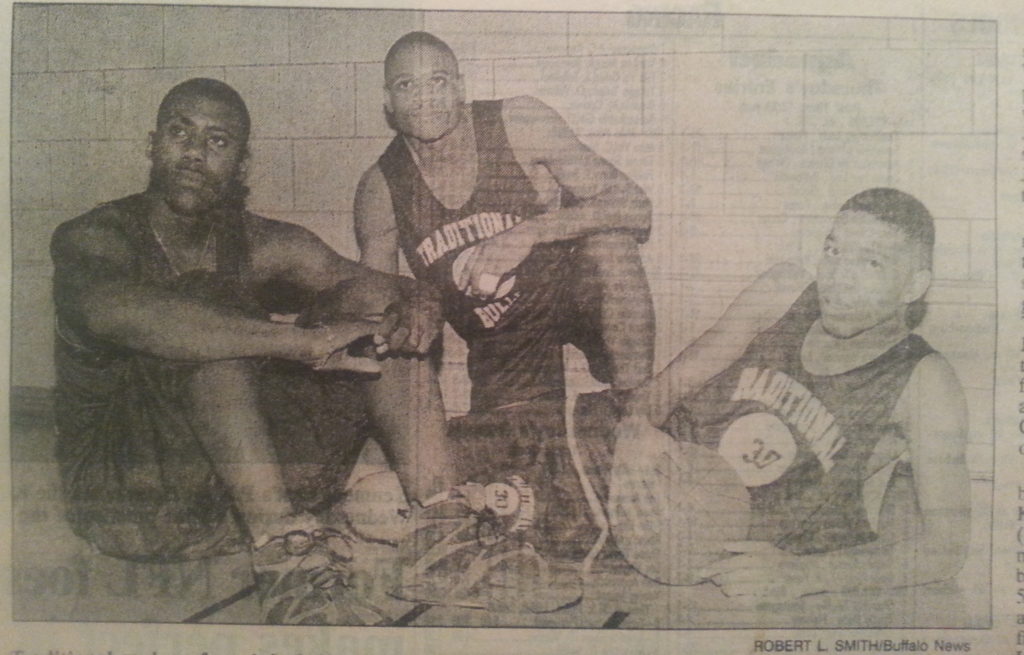

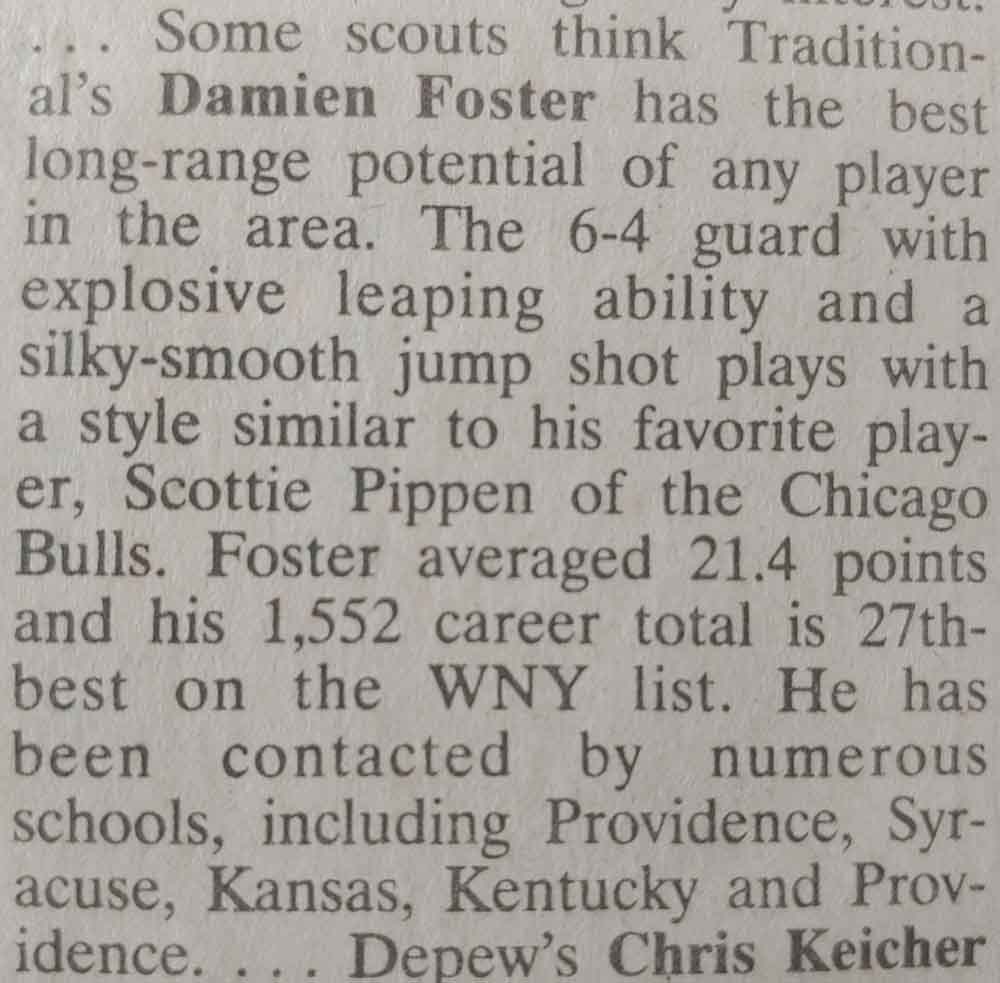

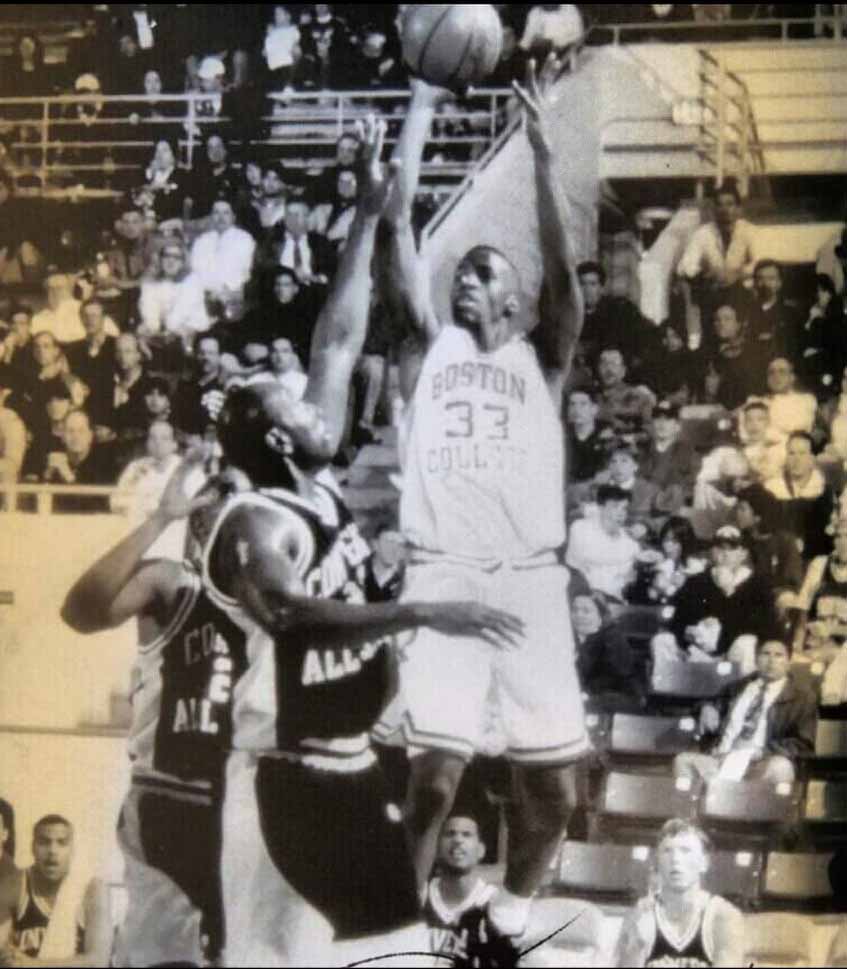

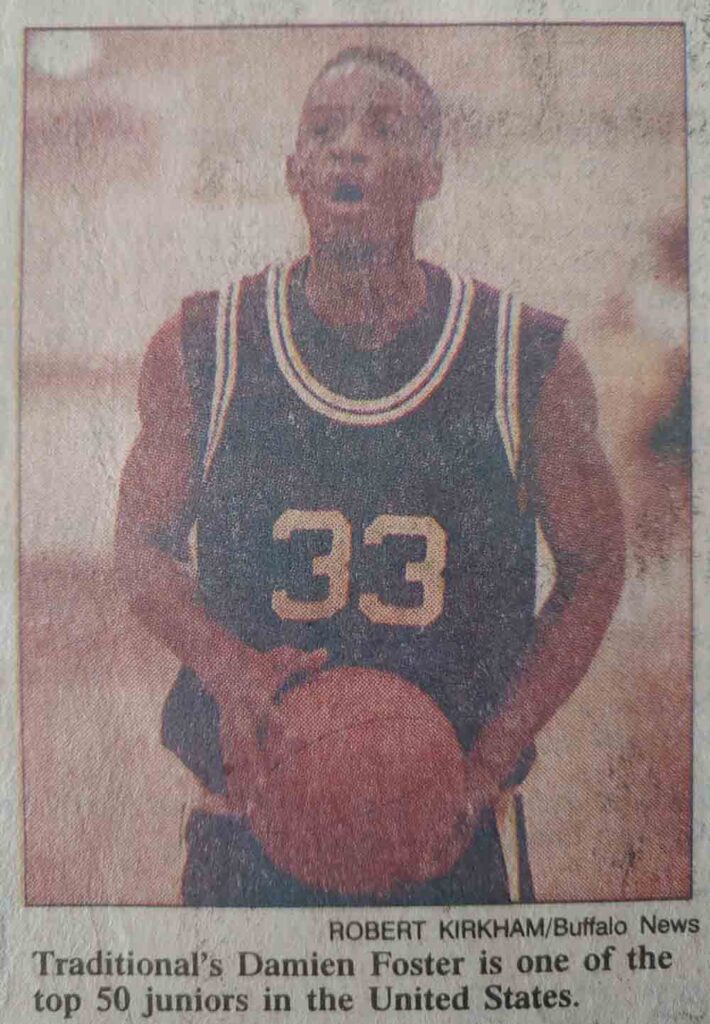

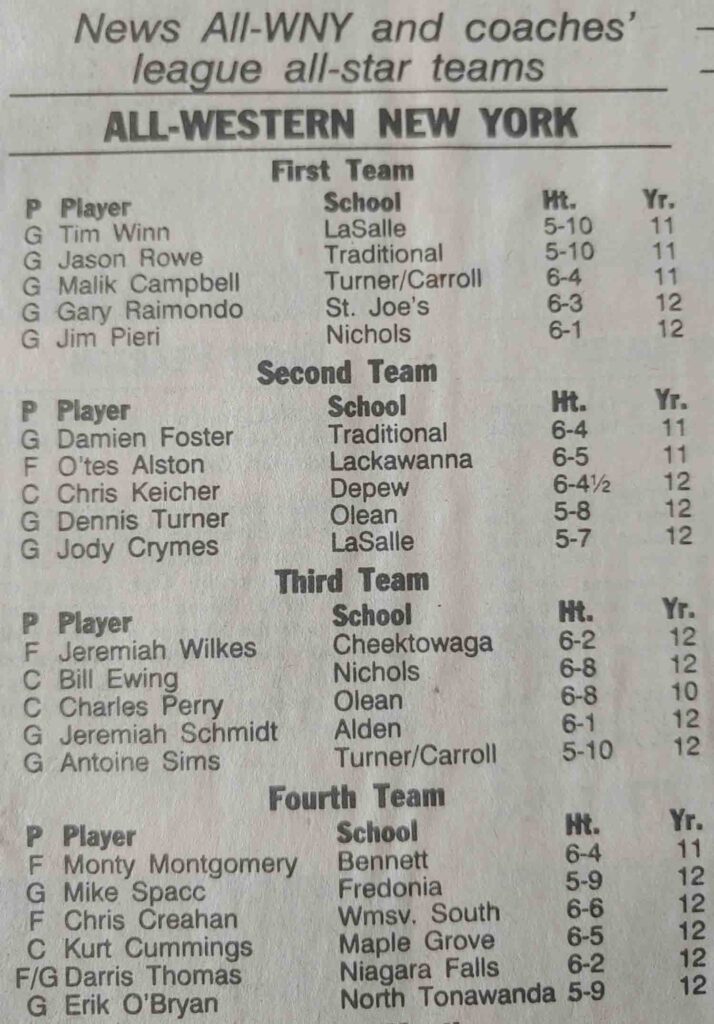

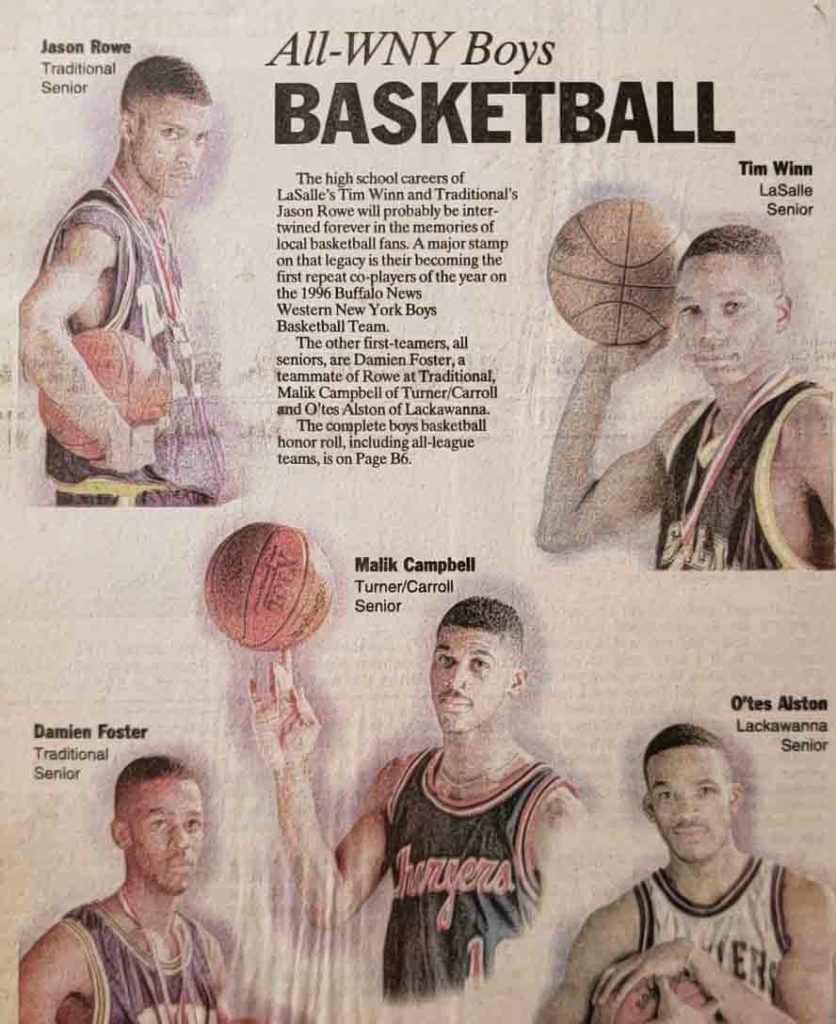

This interview is the second part of my interview with Buffalo basketball legend Damien Foster, the other half of the Buffalo Traditional dynamic duo from the 1990s. In part one we discussed his background, and the run he and his teammates went on at Buffalo Traditional High School in the early- to- mid 1990s in Western New York’s city league, the ‘Yale Cup’ and in postseason play. In part two we discussed his basketball career after Buffalo Traditional at the college level. The pictures in this post were shared courtesy of Damien himself and from an archive of Section V and Section VI basketball assembled over the years from issues of the Buffalo News and the Rochester Democrat & Chronicle by my first Coach at Hutch-Tech High School, Dr. Ken Jones.

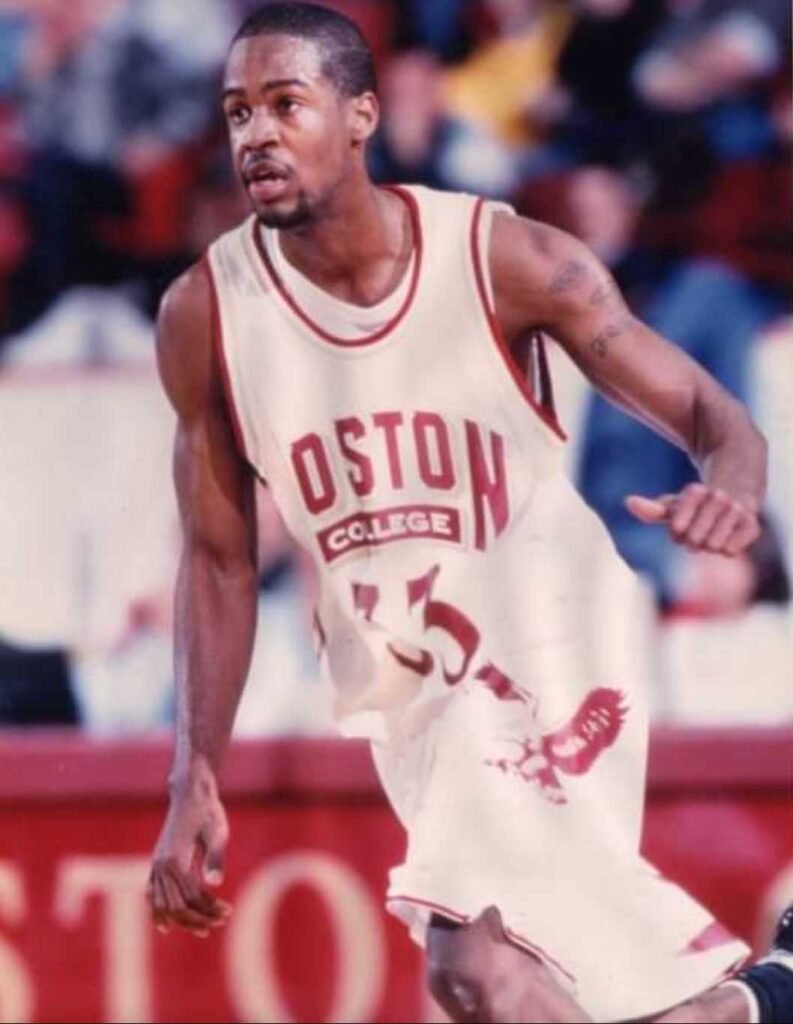

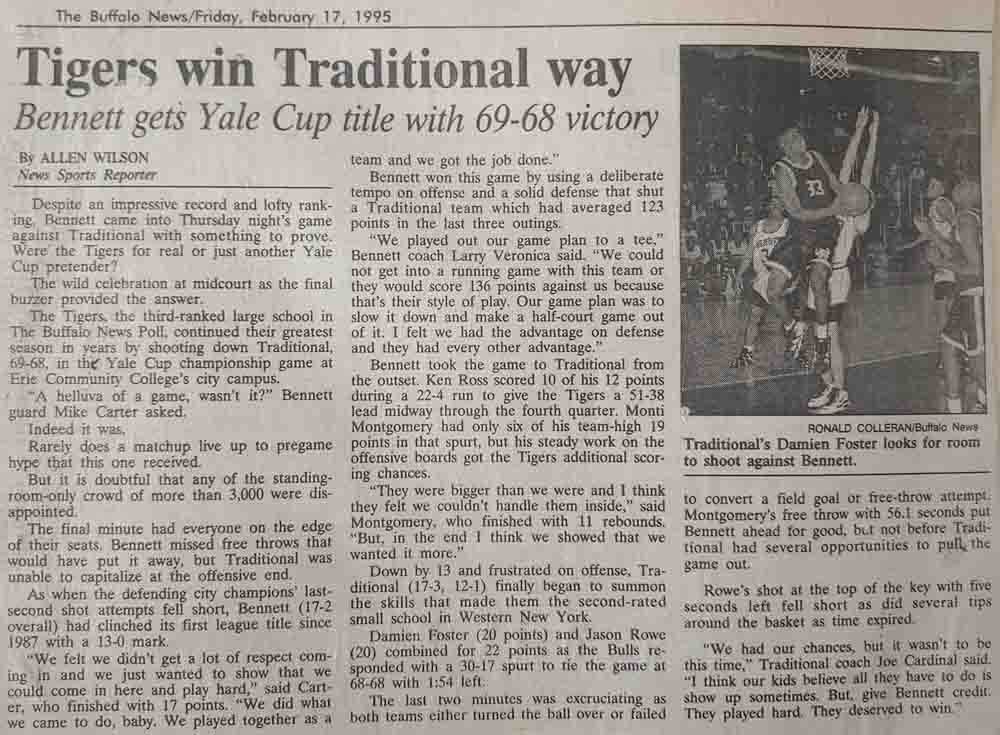

Anwar Dunbar: So pretty much after your freshman year, you guys had ‘bullseyes’ on your backs (no pun intended). Everyone was looking for Buffalo Traditional, but were there teams you guys looked forward to playing? I know there was a ‘thriller’ against Bennett High School in your junior year. Adrian Baugh (pictured below in blue) posts about that sometimes on Facebook. Did you have that game circled? I know Bennett was supposed to be pretty good that year with players like Mike Carter and Monty Montgomery.

Damien Foster: Well, in our junior year we lost to those guys. I think we took them for granted. I have that tape and I watch that game. I watch a lot of the games. I’ve got all the games starting from my freshman year. We really weren’t focused on that game and we really didn’t have a game plan, so we really didn’t know what to expect. We knew they were good, but we felt like we were going to go in, beat them and take care of business. When the ball went up, those guys were focused! Mike Carter was focused! The infamous ‘spin move’ – everyone kept saying he was spinning to the hole. Mike was a big guy! He was a football player so once he got you on his hip, it was hard to contain him. So that game caught us off guard and it really sparked the rivalry between us and Bennett.

Losing that game in front of all those people – I want to say that there were 5,000 to 6,000 people at Erie Community College’s (ECC) gym at the time, it was very embarrassing. Those guys rubbed it in our faces, and it was one of those things like where you say, ‘Wow.’ They definitely had a bullseye on our calendar for next year. I was absolutely looking forward to that game and I couldn’t wait for it in my senior year. You could tell the difference between our junior and senior year – the focus was just so different. We were locked in my senior year. There was no way they were going to beat us again. Some of their players didn’t care for me – Monty Montgomery didn’t care for me. I didn’t care for him and that was a rivalry. It was what it was, but yes, that game for sure.

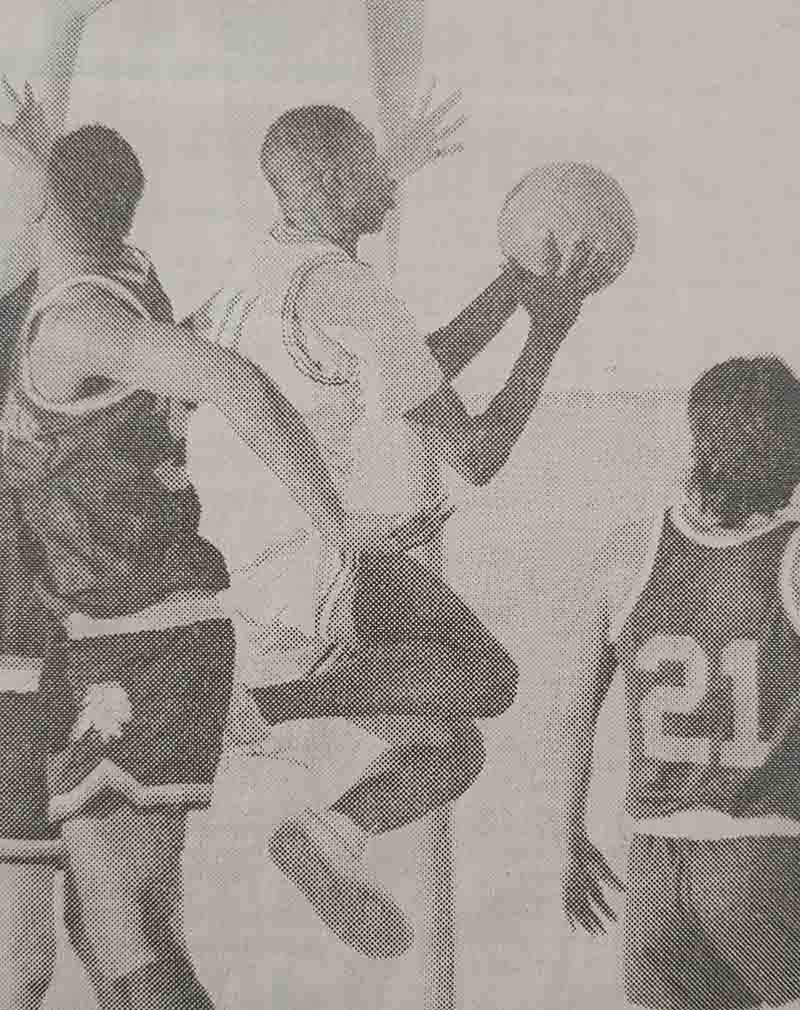

I looked forward to playing against Jeremiah Wilkes and Burgard High School (pictured). I also looked forward to playing against Kensington High School, which had Kilroy Jackson and Edmund Battle. You couldn’t just go into Kensington and be soft. Edmund Battle and those guys would talk crap to you and try to intimidate you. Me? I liked it because it got me going and those were the games I looked forward to playing – the big games against guys who talked crap – guys who thought they were tough. It was definitely Kensington, Burgard and Bennett. Those were the teams.

AD: Now, I might not put this in print, but did you and Monty have some kind of run in at a summer league?

DF: No. Monty moved here from California and he was on his California ‘swag’. He talked about how he was going to do this and do that. He looked at us like, ‘Who are these guys?’ I’m looking at him saying, ‘Numbers don’t lie!’ And there were some words that were said over the summer when he first got here. And then when they won the game in my junior year, they really ran with it so that’s kind of what got the fire underneath me for my team.

AD: Well they had a bit of a ‘reckoning’ when postseason play started because they got disqualified in the Class B bracket, while you guys went on to Glens Falls and then back again. Anyway, your best game, was it the final game where you got the MVP or was it something else?

DF: For me I would say it was the state championship final game in my senior year. My shooting percentage was pretty high. I scored more points in other games, but it was just more so the timing of when the points came because it was the state championship. I won the “Most Valuable Player Award” and that was huge.

AD: I also asked Jason this. I asked him about the last shot of games, and he said it was never a concern because your team were usually so far ahead of your opponents (laughing). In terms of the volume of shots, were you always able to find a balance?

DF: You’ve got two ‘A-type’ personalities, two ‘alpha-dogs’ out there – of course you’re going to bump heads a little bit. Me and Jay (pictured with Damien), we were close, so we knew how to work through it. It was never a concern about who would take the last shot because we were both comfortable with whoever shot the ball. If one of us ‘squared up’, both of us had a good chance of the shot going in. We both had great shots, so for me, I never had a problem with him taking the last shot and he never had a problem with me taking the last shot. It was more like just make it and get the win.

Our chemistry was always natural from our playing together at the Boys Club, learning the game together and coming up together. We were cut from the same cloth. Teammates are going to argue. You’re brothers and you’re around each other all the time – the locker room, practice, school. When we were on the court it was a family and it was all about taking care of business.

AD: Of your four years, was one your favorite or did you enjoy them all together?

DF: I enjoyed all four years, but my senior year was my favorite because we won everything. We won the Yale Cup, the states and the federation. It was just a great year. There was a lot of winning and when you’re winning, everybody is happy. You’re being remembered, you’re writing your legacy and you’re winning at the same time. It was my best year, but then you hate for it to come to an end because you know it’s your last year. The years go by so fast.

AD: With your team coming in together, was Jason your closest teammate? Or were you tight with some of the other guys?