My blog focuses on Financial Literacy/Money. Ideally everyone will cruise through life with sparkling clean credit, but that doesn’t happen for some people. It isn’t the end of the world financially though. The following contributed post is entitled, How To Make It With Bad Credit.

* * *

A big part of discovering the truth of your finances as you get older, more responsible, and start planning for the future is that you find out your bank balance is far from the only thing that matters. Whether you’re buying a new car, trying to put down a loan on a house, starting a business, or even trying to rent or start a job, your credit can have an impact. So, what do you do if you have a bad credit history or no credit history at all? Is it really such a dead end? Here, we’ll explore your options.

One of the realities of living with bad credit is that you have fewer options when the chips are down, metaphorically speaking. You may not be able to access funds and credit cards as easily as others might, and, as such, you have to get a lot more effective with your cash flow management. Start by creating a detailed budget that breaks down all of your needs, including rent, food, and utilities, while setting aside your “wants” like subscriptions or dining out. This way, you can much more easily start cutting costs when you need to. Overspending can easily lead to finding yourself having to rely on costly measures such as payday loans.

Know Your Options When You Need Cash

The one time that you’re likely to really rub up against the truth of having bad or no credit is when you need to borrow money. Whether it’s to make house payments, to pay out for repairs, or other important expenses, there may be no alternative but to get the cash that you need. However, your credit score is not the only thing that you rely on. For instance, you can compare secure loans that may allow you to put down some collateral, such as property or vehicles. This can allow you to still get access to loans with reasonable repayment terms, just make sure that you’re borrowing with intention, paying in full what you owe, when you owe it.

Build Your Credit Score

The reality is that as long as you have bad credit or no credit history, you’re going to be at a disadvantage. Having options is good, but having more is better, so you need to improve your credit card score. Paying all of your bills before their due dates to build up a solid payment history, reducing your existing debts, and being mindful about when and why you open credit accounts can all help you steadily build up your score. Be sure to get a free credit report check so that you can keep an eye out for any marks on your record that could be disputable, as often companies can get it wrong and penalize you for something that isn’t actually your responsibility.

Bad credit does not have to be the be-all and end-all of your financial potential. However, it doesn’t matter a lot. For that reason, you should start working on improving it with the tips above.

A key focus of my blog is Financial Literacy/Money. While your credit score isn’t necessarily the be all and end all for your personal financial health depending upon your own unique circumstances, it’s definitely better to have a good score versus a bad score. If you have a lower credit score and want to raise it, it’s absolutely doable. The following sponsored post is entitled, 3 Tips for Raising Your Credit Score.

* * *

Your credit score is important as this number is often what qualifies you for the loans you need to make big purchases. Unfortunately, many people have subpar credit score due to having too much debt. It is never too late to work on improving your credit score so if you use these three tips, you can boost your score so you can qualify for large loans in the future.

Pay Off Debt

Paying off debt is the simplest way to improve your credit score but it can be difficult to do when you live paycheck to paycheck. Start by tracking your monthly expenses and creating a budget. Then make sure you have paid all of your bills and place any extra money you have on your lowest credit card bill. Paying more than the minimum payment will help you pay off the card more quickly.

Keep Lines of Credit Upon

One of the biggest factors for your credit score is the ratio of debt to available credit. The higher this ratio is, the lower your credit score will be. For this reason, it is a good idea to keep lines of credit open even after you have paid them off. Your credit score will increase as debt goes down and you have more available credit for each of your cards.

Monitor Your Accounts for Fraudulent Charges

While most credit card companies catch large fraudulent charges to your account, they may not notice small charges that add up over time. If you aren’t monitoring your accounts, you may find yourself paying for these charges without realizing it. Make it a habit to check each of your accounts regularly so you can initiate a charge review if you have any fraudulent charges.

Improving your credit is a lengthy process but it can be done. Use these three tips to get started.

Two of the focuses of my blog are Current Events and Financial Literacy/Money. The Coronavirus/COVID-19 Crisis/Pandemic has thrown many people’s personal finances into chaos. One avenue for managing this economic hardship is borrowing which can actually confound matters. The following contributed post is entitled, Advice On Borrowing Money Because Of Losses Due To COVID-19.

If you are thinking about borrowing money, you need to do so with a great amount of care. This is especially the case during the current pandemic. However, a lot of people have found themselves in a position where they need to borrow money. This is especially the case for those that are not eligible for government assistance. In this blog post, we will talk you through some options that are available, as well as providing some advice. It is important to be aware that there is no one singular borrowing solution that is great for everyone. You need to make sure you can always make the repayments, otherwise, you could find yourself in a much bigger cycle of debt.

Unfortunately, the need to borrow money is something most people experience. If you don’t have rich grandparents or generous friends, the only other option is to borrow money from a financial institution or a lending company. Nonetheless, there have been many horror stories of individuals who have taken out a payday loan for example, and then struggled to make the monumental repayments. If you are borrowing money you have to be extremely careful regarding the path you go down.

A credit union is the best place to start The best place to begin when it comes to borrowing money because of losses you have incurred during COVID-19 is with a credit union. Joining a credit union means that you will essentially be part of a community whereby people are encouraged to save, and lenders lend to other members when they are in need.

There is no guarantee that joining a credit union is going to be an option for you. You will only be able to secure a loan if you are a member. There are a lot of credit unions that are going to require you to save first before you can opt to take out a loan. However, this is not always going to be the case, so it is certainly worth looking at the different credit unions that are out there and seeing whether you will be accepted into any of them.

If you can’t join a credit union, what about a loan secured against your vehicle? There are many loans to choose from, however, car logbook loans are popular with a lot of people to help them through the COVID-19 financial strain. One of the best things about a logbook loan is the fact that almost everyone can apply. This does not mean everyone will be approved, however, it does mean that there is hope for those with a bad credit history. If you wish to take out a logbook loan you will need to be over the age of 18-years-old, the car must be in your name, and it must be paid for in full. In addition to this, you have to show that you are going to be able to make the repayments. Nonetheless, credit history checks are not always carried out, and therefore if you have a bad history you needn’t be fearful. There is every chance that you may be accepted if you meet the other criteria put in place.

In addition to this, if you take out this type of loan you will still have access to your vehicle. A lot of people worry that they have to hand over their car until they have paid the money back. This is definitely not the case. The only time the company can take your vehicle is if you fail to meet the terms that have been outlined in the contract. Otherwise, you can continue to live life as normal.

A lot of people like car logbook loans because of the easy application process. If you were to borrow money from a bank, for example, it is likely that you would experience an extremely segmented process. You would have to hand over one document, then come back and fill out several forms, then you will be asked for further documents, then you will need to wait for something to be checked, and so on and so forth. It seems to be never-ending. However, with a logbook loan you are usually only required to fill out an application form online and you will be informed of everything you need to provide prior to doing so.

Last but not least, this article would not be complete without mentioning the amount of money you can borrow and the repayment terms put in place. Flexibility is undoubtedly the name of the game when it comes to this type of lending. There are so many companies offering logbook loans and therefore you are assured to find a loan that fits in with your circumstances and your needs. In addition to this, you only borrow what you need. This lessens the risk of you experiencing any difficulty when paying back the cash.

What happens if you have a bad credit history? Let’s clarify the fact that there are criteria in place you will need to meet when applying for any type of loan. A lot of people have a tendency to assume that anyone with bad credit will not be accepted, but this is not the case. Nevertheless, what makes some of the online loan companies different from traditional lenders is the fact that they do not consider your credit rating first and foremost. If you were to apply for a loan from a bank, for example, you would need a good credit rating to get past the first stage. However, some online lenders are more bothered about the current monetary situation you find yourself in, rather than any mistakes you have made in the past.

They want to know that you are going to have the ability to make the repayments every month, and this is why they want to see that you have a regular income coming in. This is their main priority. This does not mean that your credit rating won’t be considered; some direct lenders will conduct a credit check as well. Nonetheless, this does not necessarily mean that your bad credit rating is going to hold you back. There is every chance that you will be approved if you show the lender you are someone trustworthy to lend to.

Two of the focuses of my blog are Financial Literacy/Money and Business/Entrepreneurship. There are many people who don’t understand credit. While letting something like credit card debt get out of control can be damaging to one’s personal finances, it’s important to obtain and maintain a solid credit profile. It has implications for your personal finances and ability to start a business if you have entrepreneurial aspirations. The following contributed is entitled, Credit Invisibles: How to Build Your Credit Profile.

* * *

Many individuals are “credit invisible.” This means that they don’t have enough relevant information in their credit reports to produce a credit score. If you find yourself falling to be in this category, it can be impossible to apply for loans or credit cards, get a mortgage, or even land a job. Here are some proven ways to build your credit profile and establish a history.

Make use of alternative data

Credit scores are usually generated based on comprehensive repayment histories or credit reports. If you lack these, it’s possible to generate a score based on alternative data and supplemental information like utility, cellphone, and rent bill payments. Even without a history of repaying home, student, or auto loans, you’ll now be granted access to a credit score through alternative data credit scoring. It also works if you have a credit score that has been previously damaged. This kind of data will be able to produce a credit assessment that is highly predictive and unlike traditional credit scores.

Affiliate yourself with a community bank or credit union

Join a local credit union and take out a small signature loan or credit-builder loan. With these kinds of loans, the local bank or credit union will first place your loan money into an interest-bearing savings account which you’ll make payments to. Your payments and activity will get reported to the credit bureaus. Once you’ve fully repaid the loan, you’ll be able to receive the money and you’ll have built up an adequate repayment history.

Add yourself to an existing credit card account

Seek the help of a family member or loved one who possesses a long-established, positive credit history. Ask if they can add you to their credit card account as an authorized user. The older their credit card, the better since the information that dates back to when the card was first opened is included on the user’s credit file. Once you become an authorised user, you’ll be issued a card, but you won’t need it to make a credit history. This card is directly linked to the primary cardholder, and they’ll be responsible for the charges made on it. It’s best not to use it at all so that you can avoid getting into any conflict with them. Check your credit score when you’ve had it for several months. If your credit score is at 670 to 740, then you can apply for your own card.

Make a request for a secured credit card

Applying for a secured credit card doesn’t require a credit score, but it does require you to put down a refundable deposit which will serve as your credit line. This means you’ll be borrowing against your own money. If you’re unable to cover payments, the lender will take money from your deposit in order to repay it. Make sure to use the card sensibly by only charging small items on it that you can afford to repay in full by the due date. This will allow you to build a positive credit history in just a couple of months.

Besides paying your bills on time and applying for high-interest, short-term loans or cards, these simple methods will help you go from a non-existent credit score to a great one.

Two of the focuses of my blog are Financial Literacy and Money. Building and maintaining a strong credit rating can significantly affect one’s financial health and open certain doors and opportunities. The opposite is also true. The following contributed post is thus entitled; Your Credit Report Tells Your Life Story.

* * *

Over 65% of job applicants admit to embellishing the truth on their resumés. LIttle white lies here and there and optimistic descriptions of their tasks can move your profile from being at the bottom of the list to the top on the recruiter’s desk. If there’s one thing that most adults spend a lot of time improving, it’s their professional profile. So it’s surprising that less than half of the population care about their credit score. Indeed, almost 30% don’t know their credit score and don’t really see how it can affect their everyday lives. The most common interaction with the credit score is to check whether or not you are eligible for a specific loan or credit card agreement. Consequently, it appears crucial to draw a parallel with your professional profile. Indeed, in the same way than your resume can influence your career; your credit score can equally affect your financial situation. More importantly, you can manage what your credit score reveals about you.

It’s a number, but it says a lot about finance management

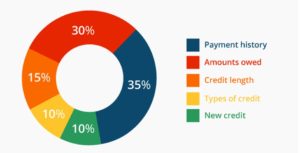

The scale of the score for your credit report goes from 300 to 850 – although you can find specific credit card scoring systems that start at 250 and runs to 900. Ultimately, while it’s fair to say that a number might be meaningless at first, you need to understand what it means. Potential lenders and employers can ask to see your score and make an informed decision to trust you or not based on the data available. Ultimately, a score in the highest part of the scale, 781 to 850 implies you’re responsible with your money. While a score in the lowest range of the scale, 300 to 600 can put lenders and some employers off, as it shows you’re not managing your finances.

Mistakes remain visible for long

Unfortunately, lenders don’t only check your credit score, but your full report. The report is the equivalent of your financial resume. It shows all the major decisions you’ve made and can highlight some of your issues with debts or the law for several years. However, you can clear up your report gradually. If you’re worried about the time it takes to remove judgment from credit report information; you might need to get in touch with a legal expert to find out more. More judgment items are removed after 7 years from the date the lawsuit was filed, but there are exceptions. Additionally, some credit bureaus and creditors might choose not to report or mention all negative items.

People look at your finances, not your social privileges

Ultimately, there is an essential element that your credit score encourages. While a resume can suffer from stereotypes based on the education you’ve received or your race, a credit score is, as you know, only a number. The report might highlight your financial strategy and preferences, but more importantly, it showcases your priorities and the time you invest in finance management. Where discrimination is still present in the workplace, credit reports focuses on facts. Being only a number saves you from unfair preconceptions.

The bottom line, for many newcomers to the finance world, is that your credit report is not an enemy you should fight. It’s an opportunity for self-improvement – when the score is low – and for unbiased achievements. Your credit report might shut some doors but, in the grand scheme of things, it helps you to access opportunities that social, racial and gender discriminations would have made more difficult to reach.

Two of the focuses of my blog are Financial Literacy and Money. Building and maintaining a strong credit rating can significantly affect one’s financial health and open certain doors and opportunities. The opposite is also true. The following contributed post is entitled; 5 Ways You Didn’t Know Your Credit Rating Would Affect Your Life.

* * *

Ah, credit rating. You have probably heard the term in financial circles when dealing with mortgage applications and cars, but your credit rating can have a huge impact on your life – even when you didn’t realise it. Most people don’t tend to concern themselves with their credit rating – particularly young adults, who believe that a credit rating is something for homeowners and richy rich people to worry about.

Credit can have an effect on the way that you do everything. If you choose to go back to school, for example, you may need a finance loan to help you to pay for your living expenses. If your credit isn’t great, you could find yourself instead turned down for mainstream finance and turning towards loans for bad credit instead. This is a good way to start building your credit from the poor to the good, but it’s not always that simple for everyone. So, with all of that in mind, how DOES your credit rating affect your life?

Buying Property

It’s an obvious one, but you will find it very difficult to be approved for a mortgage if you have debt on your credit file. You need to clear the debt on the file to start improving your credit rating, otherwise you could find yourself with a very high interest mortgage instead of one you can actually afford.

Owning A Business

If you are aiming to own a small business, credit can really affect your ability to ensure that your business can stay afloat. You may not be the sort of business that needs external funding to start with, but that doesn’t mean that you won’t need it later. Personal bad credit can affect your business credit.

Getting A Phone

No one can live without a smartphone these days, well, you could but it’s not the norm anymore. The thing is, electrical items like this are never usually bought outright; they’re bought on finance. If you don’t have the right credit rating, you can be turned away from getting that contract.

Utility Bills

You need to access water, electricity and gas. If your credit rating is poor, there is a chance that you could be put onto special metres for your payments because the companies would see you as not being trusted enough to pay those bills on time. These metres are often higher in cost to run. Good credit can save you cash every month.

Property Interest Rates

The amount of interest that you can secure on your mortgage is directly linked to your credit rating. So, we mentioned earlier about having trouble buying a property, but if you manage to secure finance, your credit rating can push that interest rate right up.

The key to your credit rating is to work out how to pay off the debts that you owe and gently start improving the rating that you have. Once you start to do this, you can rebuild your credit with a bad credit loan and make efficient payments to prove you can do it.

Two of the main focuses of my blog are Financial Literacy and Money. The following contributed post was written by Emma Morgan. It discusses The Signs You’re Carrying Far Too Much Debt.

* * *

We live in a time of consumerism and most of us have a mindset of ‘I need it now’, which makes us impulsive when it comes to credit. The problem with credit, though, is that we can have whatever we want, and the consequences come later. While credit seems like a great idea in the moment, when you’ve got too much month at the end of your money and you can’t make your repayments, it becomes a big problem.

Debt is, for most people, a very unfortunate part of life. Buying a house, a car and even getting an education can put you into debt. While these are the debts you’d want to have, rather than because you couldn’t put the Manolo’s back at the store, it’s still not nice to have to deal with debt in that way. Having a house is a good thing, until you can’t make the mortgage repayments and you’re getting help from DoveBankruptcyLaw.com/chapter-13-bankruptcy to get you back on track. There are some signs, though, that can tell you whether you are carrying too much debt. It’s time to get your head out of the sand and start sorting out your finances, because they’re not going to sort themselves.

1. The first sign you’re carrying too much debt is that this is where your money goes. You should have enough money to cover your mortgage, your bills and your savings before having a portion for disposable income. If your disposable income is covering the minimums on your loans and cards, there’s an issue. Working to pay debt is not living, and you need to start making some adjustments so that this is no longer the case for you.

2. The next sign is that you won’t ever pay off your debts early, because the money that you have can only cover the minimum payments. Get onto the creditors that you have and ask them to lower the repayment amounts for you. Creditors are not easy to deal with – in your head. In reality, if you have a good history, they’re usually more than happy to help you out. As long as they are getting paid, they will work with you and not against you.

3. Your health is important, but if the stress of debt is starting to manifest physically, you’re going to suffer. Your sleep, your happiness, the jumpy feeling you get when the doorbell goes? All of these things are not healthy, and they can be affected by debt.

4. Trying to get a consolidation loan to cover your debts is the move that most people make so that they can pay things off quickly. However, if you’re being turned down even for this, then you’ve got too much on your plate. The more debt you have, the harder it is to get credit.

It’s important to recognize when you are carrying too much debt as much as it is to know where to ask for help. Don’t suffer alone – get the debt help you need now to lessen the burden on your shoulders.